By Paul Mueller

By Paul Mueller

At this point, we should try to get a clear picture of what ESG advocates hope to achieve. But because there are so many different people in the ESG movement with differing priorities and values, it will be difficult to nail down any simple or universal goals. Still, we must do the best we can to understand where ESG advocates want to take us.

Environmental

While ESG advocates have a wide range of environmental goals, one goal dominates: combatting climate change. Well over half of the targets, disclosure requirements, regulations, and cost of the environmental piece of ESG comes from the goal of reducing greenhouse gas emissions. The problem of climate change dominates the environmental criteria because it is universal – everyone contributes, and everyone is affected – and because it more easily lends itself to metrics.

Global warming has the clearest and most universal goal: reduce greenhouse gas emissions. The quantity of reduction varies some by organization and industry, but every target involves one of these key metrics:

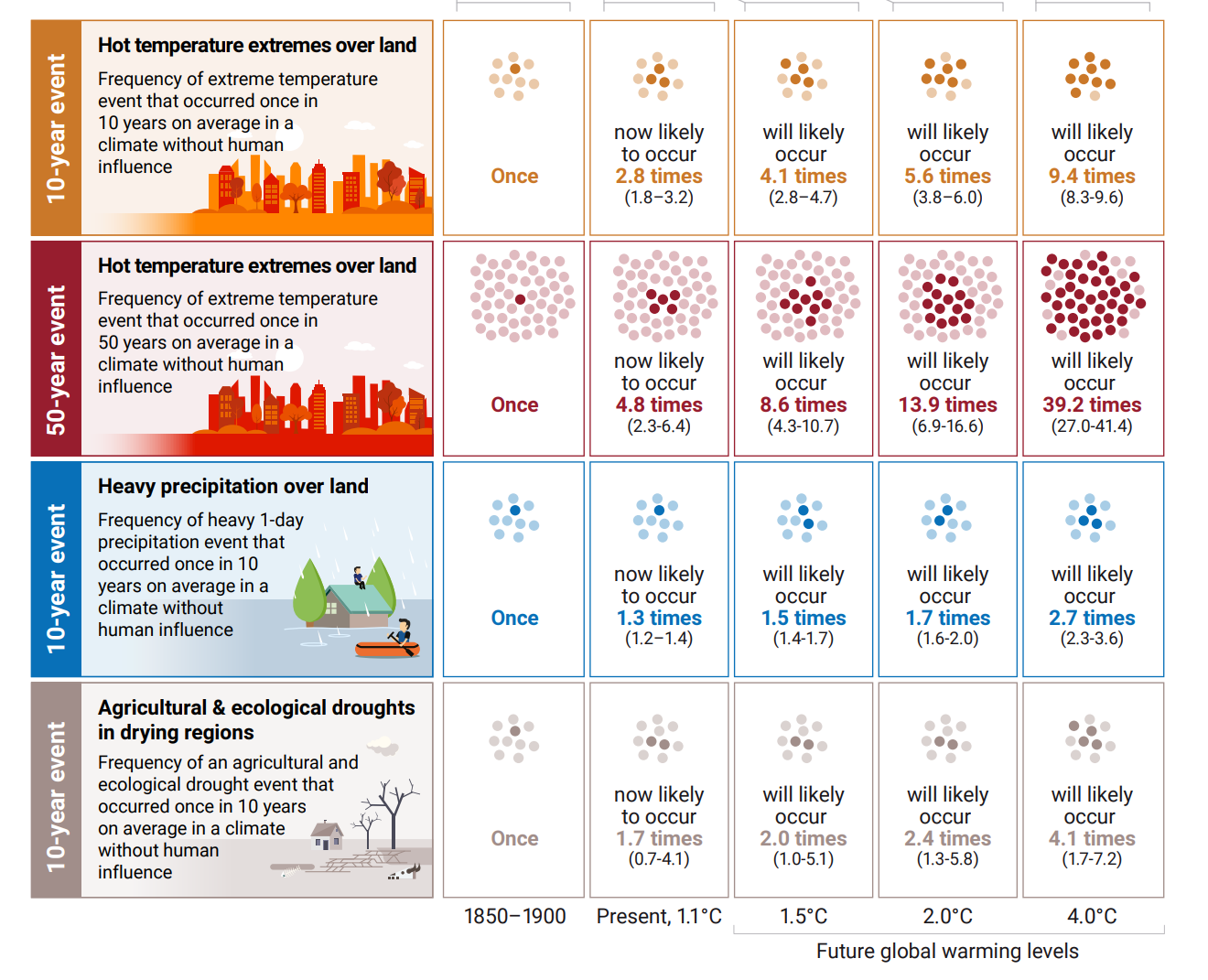

- 2030 – The Paris Agreement in 2015 set a fifteen-year benchmark. Given IPCC models and predictions, a variety of emissions reduction targets were set for 2030. The argument made by ESG advocates is twofold. First, it will be harder to slow or stop global warming the longer we wait to act. Second, the downside of global warming increases dramatically as the temperature rises. The 2023 Emissions Gap Report by the UN Environment Program, for example, claims that extreme weather events will happen more frequently the warmer the planet gets.

(pg. 32 of 2023 Emissions Gap Report)

- 2050 – This year has been set as a “realist” time frame for more aggressive targets for industries to reach net zero. It is a kind of compromise environmentalists have made with reality since it is blindingly obvious that net zero cannot be reached in most industries by 2030.

- Net Neutral – As I mentioned in my piece about ESG Terms, net neutral refers to reducing or offsetting one’s greenhouse gas emissions entirely. Carbon offsets are critical for achieving this goal. Very few industries can reduce their emissions to zero or recapture the equivalent of their emissions output. The only way they will be able to achieve net zero is by funding (buying) carbon offsets from third-party implementers. This has already created a thriving cottage industry of climate mitigation firms.

- 1.5O Celsius – In 2015, scientists at the IPCC deemed this amount of warming manageable and potentially achievable. The most recent UN report suggests that it is no longer a feasible goal. In 2015, global emissions were projected to be 16 percent higher today. Instead, they are only 3 percent higher.

Activist Post is Google-Free — We Need Your Support

Contribute Just $1 Per Month at Patreon or SubscribeStar

“However, predicted greenhouse gas emissions must fall by 28 percent for the Paris Agreement 2O C pathway and 42 percent for the 1.5O C pathway.” (pg. XV) that’s a tall order for growing economies and a growing global population! Still, most organizations use 1.5O C or 2O C as reference points for their benchmarking.

The IPCC uses specific models and makes forecasts of how much the earth will warm at varying rates of emissions. Although specific targets are chosen (1.5O C or 2O C), the models predict ranges of temperature increase and probabilities. For example, continuing with current policies, the report predicts a 50 percent chance of the world being 1.8O – 3.5 O warmer than pre-industrial times, a 66 percent chance of being 1.9 O – 3.8 O warmer, and a 90 percent chance of being 2.3 O – 4.5 O (pg. 31). They rate the probability of staying below 1.5 O warming at 0 percent except for the most optimistic case of massive reductions in greenhouse gas emissions and rapid movement towards net zero.

Of course, global temperature change, although the most salient, is not the only goal under the Environmental umbrella. Other climate goals vary by region and country. But nearly all of them revolve around using fewer resources. Water is the next most important issue after greenhouse gas emissions. Concerns about water tables, contamination, droughts, and flooding are widespread. Here are other environmental issues:

Reduction of Waste

Recent bans on plastic bags around the country reflect ESG advocates’ concern about creating waste that is not biodegradable. The entire recycling movement has been rolled into the E of ESG. Beyond that, ESG advocates want to track, and reduce, food waste and how much energy goes into food production. Besides purported health benefits, they advocate vegetarian, vegan, and other lifestyle choices because meat takes a lot more resources to produce than grains or insects. Ultimately, the ESG movement advocates people and companies using less stuff, fewer resources, and less energy.

Preservation of Resources

More traditional environmental concerns include preserving habitats, ecosystems, and biodiversity. Companies are judged by how much they disturb ecosystems – whether habitats for endangered rodents or moths. Environmentalists are also concerned about farming practices that leach nutrients from the soil and are “unsustainable.”

Aesthetics of Nature

Aesthetic environmental beauty is less of an issue for ESG, but could still fall under it. Movements to limit new neighborhoods, factories, mines, and other developments often make arguments about ruining the landscape, creating blight or sprawl, and making the world less pleasant. They don’t want to sully pristine environments like ANWR with “ugly” pipelines and drills, for example.

Reducing Harmful Pollution

Consumer protection has long been a mainstay of environmentalism – from campaigns against smoking to raising awareness of the detrimental health effects of lead and asbestos. Recent campaigns to ban gas stoves, various pesticides, and genetically modified organisms (GMOs) follow this trend. Agricultural businesses and consumer durable manufacturers are scored based on the potential environmental effects of their products – so alcohol and tobacco are dinged in their scores, as are agricultural companies that use pesticides and GMOs.

Social Goals

Internationally, social goals tend to revolve around equity – especially material (wealth) equity and equity between men and women. In more developed European and Anglo-American countries racial and gender “equality” also have great importance. While many of these values also influence the Governance category, we’ll see that the specific goals or outcomes aimed for differ between the S and the G of ESG.

I’ll do my best to cut through the jargon used to describe Social goals, but sometimes that’s really all there is to them. One set of Social goals relates to the supply chains of large corporations. Another set of social goals relates to Diversity, Equity, and Inclusion (DEI).

Worker Conditions

Certain worker conditions are considered acceptable and others unacceptable, although there is no universal or objective standard for making the distinction. A company could receive a lower score if workers in its supply chain are not paid enough (some version of a living wage), work too many hours, have overly difficult or dangerous working conditions, or do not have certain benefits like healthcare. The definitions of “too many,” “overly difficult or dangerous,” or “not paid enough” often vary dramatically by organization and individual.

ESG advocates push for significant redistribution of money, resources, power, and authority from groups who generally have more to groups who generally have less. In many ways, this is simply an extension of international aid. Companies (and countries) are supposed to improve living standards around the world – from the laborers harvesting coffee in rural Columbia to the workers making textiles in Vietnam to farmers across Africa.

Companies are expected to provide access to healthcare and education, to improve working conditions, to police abuse and exploitation, and generally to “empower” the downtrodden of the world.

Diversity, Equity, and Inclusion (DEI)

Diversity, Equity, and Inclusion is a grab bag of ideas and values that manifest differently by company. In the University of Ohio system, for example, it appeared in weighting applicants for faculty positions in part by their race, gender, or “sympathy” to inclusion: “One role in medical anthropology had 67 applicants. The four finalists include the only two black applicants and the only Native American applicant. ‘All four scholars on our shortlist are women of color,’ the committee said.”

In the Rand Corporation, DEI figures prominently on their website and influences what issues they decide to research. Their “truth decay” initiative has been steered towards supporting “DEI and the same progressive view of disinformation the Biden administration used to justify a massive censorship enterprise.” For the Pentagon, it involves spending hundreds of millions of dollars on consulting and “education” programs “aimed at furthering DEIA [Diversity, Equity, Inclusion, and Accessibility], and incorporating DEIA values, objectives, and considerations in how we do business and execute our missions.”

And we are all too familiar with moves by Hollywood to bring “underrepresented” groups to the movie screen – primarily based on one’s skin color or sexual orientation; not one’s political views or religious beliefs.

DEI advocates claim they are reversing past racial and gender discrimination by hiring and advancing “disadvantaged” people. As with everything else, the ESG movement has created categories and definitions for “disadvantaged.” Intersectionality designates social, racial, and gender groups as oppressed or not oppressed. Some people might be part of one or two groups. Others might be part of four, five, or six.

The clout of intersectionality comes from the fact that you can simply designate whatever group you want as “oppressed” to increase their standing or worthiness of elevation. This means those who have the authority to designate groups as oppressed or not will wield a significant amount of influence in societies that advocate Social criteria.

Besides advancement, DEI initiatives include policing speech and “discrimination” within companies. Hence the rise of signs like “hate has no place here” and “LGBTQ+ Friendly.” Affirming and advocating for the “oppressed” becomes a sign of distinction for companies and managers in an ESG framework.

Governance

When it comes to moving the ball down the field, Governance is the most important player in ESG. Advocates work to change the composition of boards and the rules, guidelines, and expectations for board members. ESG advocates push for more ethnic, racial, and gender diversity on boards. They also want more interest groups like labor unions, climate activists, and others to have board seats. For example, the Institutional Shareholder Services (ISS) claims that there should be at least one woman and one member of a minority on a board. Otherwise, ISS recommends, shareholders vote against the recommendations of the current board.

ESG advocates have made significant inroads in the investment community from shareholder research organizations like: ISS, S&P Global, and MSCI to massive institutional investors like Blackrock, Vanguard, and State Street. These organizations have been making concerted efforts to influence the boards of the largest and most important companies in the world. One can attribute the rise of “Woke” capital in large part to their activism.

But governance extends beyond promoting DEI and Environmental issues within the firm. ESG advocates want companies to work towards these goals in the broader society. We saw this at work in 2016 when companies threatened to boycott states that implemented religious liberty laws that failed to grant sufficient “protections” to LGBTQ groups. From PayPal changing its plans to expand in North Carolina to the NFL and Disney saying they would take their business out of Georgia, dozens of large public companies used their economic clout to pressure politicians on social issues.

We can also see this approach to governance manifest in the corporate response to George Floyd’s murder and the Black Lives Matter (BLM) movement. Recall how many large corporations chose to make public statements about the incident. And recall the massive contributions made to BLM that year – over $90 million in total from large companies including “Amazon, Microsoft, Nabisco, Gatorade, Airbnb,” etc. Commenting on social issues, boycotting states, and transferring significant financial resources to activist nonprofits, naturally follow ESG advocates’ desire to transform all of society.

ESG advocates want to see Governance change at the legal and regulatory level. They advocate changing the legal fiduciary duties of managers – managers of companies and managers of investment and retirement funds. In the U. S., maximizing returns has always been the north star of corporate governance. ESG advocates want to see that standard weakened or changed into a “stakeholder” model. They want boards and management to “represent” stakeholder groups and advance their interests.

While they argue such a change will be for the “greater good” of society, it will really just make corporations more malleable and subservient to the most vocal and best-organized interest groups – which at this point is the ESG movement. Besides implementing Environmental and Social goals within their firms, management with strong “Governance” ought to be an “ally” of the disadvantaged. They can do so by giving money to organizations that “advocate” for the disadvantaged, such as Black Lives Matter or the Environmental Defense Fund.

On a related point, Governance scoring can involve evaluating who and what political campaigns companies contribute money towards. Contributing towards advancing ESG laws and regulations is rated highly (in an obviously self-interested and self-referential way) while spending to oppose things like emissions reporting and reduction, merit-based hiring, and separation of business activity from social or political advocacy, are signs that governance is lacking.

Supposedly shareholder returns and enterprise value will be advanced by ESG goals. Advocates claim that climate change represents a “material risk” to companies, which creates an obligation for them to assess and report their environmental impact. Poor social standards, ESG advocates claim, lead to worse employee performance, higher turnover, and the risk of costly lawsuits. Poor governance, they say, can detract from the firm’s reputation and create risks of consumer boycotts or capital divestiture campaigns. ESG criteria, therefore, are in the firm’s and the shareholders’ best interest.

Such are the claims of ESG advocates. Yet this is largely a bait and switch, as we can see with Disney and Budweiser. Both companies engaged in activities that relate to stronger Governance according to ESG criteria, yet generated just the opposite results ESG advocates promised. Remember, ESG was initially pushed (and still is with regulators) as a valuable framework for reducing risk and increasing enterprise value.

After Budweiser ran a commercial with influencer Dylan Mulvaney, public backlash caused its share price to decline by over 20 percent from $67/share in March to under $54/share in June. In the last month, the stock has recovered significantly to about $63. But that is cold comfort for shareholders who sold or who would like to see less volatility in their portfolio.

Disney’s case is even more striking. After the company waded into the “Don’t Say Gay” kerfuffle in February, March, and April of 2022, its stock price fell from $150 to $100 within a few months. Disney has other challenges too, not the least of which is its recent string of politically correct but poorly performing movies. Its price earlier this week was in the low $90s.

It seems a stretch, to say the least, that ESG goals are primarily about shareholder value and enterprise value. They want to accomplish many other goals which are often counter to the interests of shareholders and large segments of society.

Source: AIER

Paul Mueller is a Senior Research Fellow at the American Institute for Economic Research. He received his PhD in economics from George Mason University. Previously, Dr. Mueller taught at The King’s College in New York City.

His academic work has appeared in many journals including The Adam Smith Review, The Review of Austrian Economics, and The Journal of Economic Behavior and Organization, The Journal of Private Enterprise, and The Quarterly Journal of Austrian Economics. He is also the author of Ten Years Later: Why the Conventional Wisdom about the 2008 Financial Crisis is Still Wrong with Cambridge Scholars Publishing.

Dr. Mueller’s popular writing has appeared in USA Today and Fox News, as well as the Intercollegiate Review, Christian History, Adam Smith Works, and Religion and Liberty, among others.

Dr. Mueller has given talks and led colloquia for a variety of organizations including Liberty Fund, the Institute for Humane Studies, the Intercollegiate Studies Institute, and the Russell Kirk Center for Cultural Renewal.

Dr. Mueller is also a Research Fellow and Associate Director of the Religious Liberty in the States project at the Center for Culture, Religion, and Democracy. He owns and operates a bed and breakfast (The Abbey) in Leadville, Colorado where he lives with his wife and five children.

Become a Patron!

Or support us at SubscribeStar

Donate cryptocurrency HERE

Subscribe to Activist Post for truth, peace, and freedom news. Follow us on SoMee, Telegram, HIVE, Minds, MeWe, Twitter – X, Gab, and What Really Happened.

Provide, Protect and Profit from what’s coming! Get a free issue of Counter Markets today.

Be the first to comment on "A Short Guide to ESG: Goals"