By Tyler Durden

By Tyler Durden

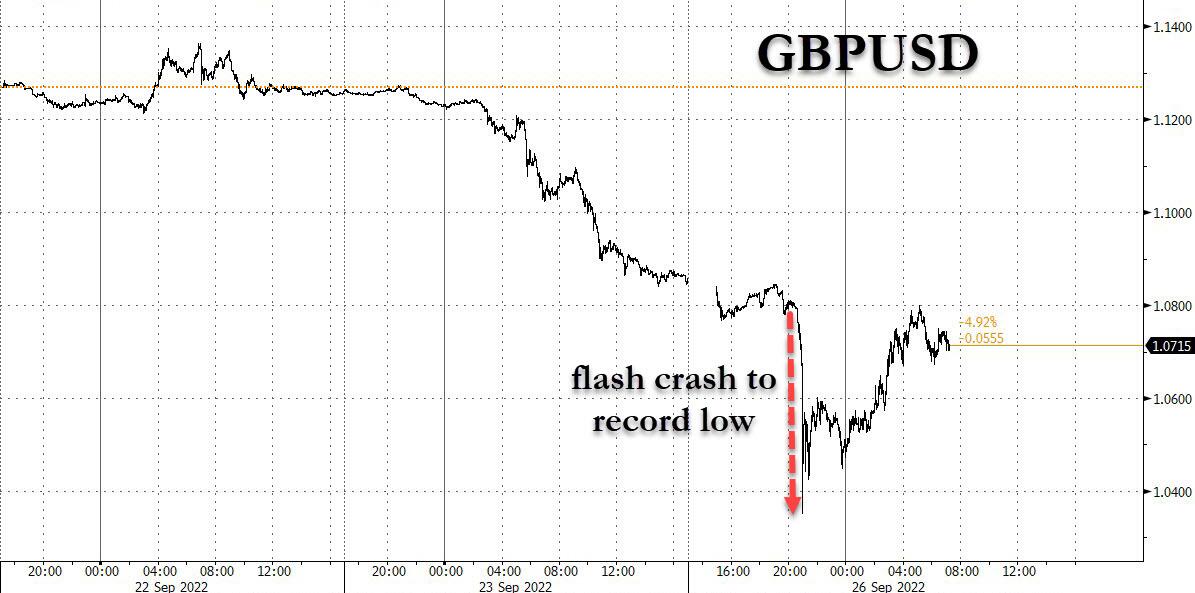

The rout which hammered stocks on Friday, nearly pushing them to close at a new 2022 low, resumed overnight when the global FX crisis returned with a bang, and a flash crash in the British pound which as noted late last night, plummeted 500pips in thin trading, to fresh record lows following Friday’s shocking mini-budget announcement which confirmed the UK has no idea what it is doing and will cut rates and issue more debt just as the BOE is desperately trying to tighten financial conditions.

The plunge in cable was, however, just one symptom of a bigger malaise, namely the relentless surge in the dollar which overnight hit fresh record highs as the BBDXY rose as high as 1,355 before briefly fading the surge…

… as every dollar-denominated debt issuer in the world is suffering crippling pain and begging Powell to do something to ease the unprecedented shock of the strongest dollar in history just as the world slumps into a global depression.

… as every dollar-denominated debt issuer in the world is suffering crippling pain and begging Powell to do something to ease the unprecedented shock of the strongest dollar in history just as the world slumps into a global depression.

Alas, so far there is nothing but silence from the Fed – which will likely have to make some announcement on central bank currency swaps at some point before the open today to avoid an even more epic FX rout – and as traders await something to break big time across global markets…

This is the week of the barbell trade: deep OTM calls and puts as things either break or CBs panic.

— zerohedge (@zerohedge) September 26, 2022

… this morning futures have tumbled another 0.7%, as eminis drop to 3,683 while Nasdaq futures are down 0.8% to 11,290 on fears that Federal Reserve rate hikes to combat persistently elevated inflation will crush the economy into a full-blown recession, or depression, and the VIX soared above 32.

It wasn’t just FX and stocks crashing: British bonds also cratered as yields surged to the highest in more than a decade, sparking talk of emergency action by the Bank of England. For one example of the total chaos look no further than 5Y UK Gilts which have exploded 51bps higher and last traded around 4.58% as the market now prices it in.

Gold and Silver: Industry-Best Customer Service at Money Metals (Ad)

Similar implosions were observed in US TSYs, where the 10Y traded just shy of Friday’s mini blowout, and was last seen at 3.7828% as bond traders are hit by VaR shocks at the same time in every possible market.

Turning back to stocks, the rout wasn’t isolated to just one market and an index of global stocks traded to the lowest since 2020. European equities extended declines after sliding into a bear market on Friday, with mining and energy stocks underperforming as metals and oil fell.

“We’re in a period of global gloom, with pessimism blanketing different countries for different reasons,” said Ed Yardeni, president of his eponymous research firm, who warned of growing storm clouds for the US economy. “The latest data jibe with our growth recession scenario, but the risks of a full-blown recession are obviously increasing,” he wrote in a note Monday.

In premarket trading, major US tech and internet stocks including Apple, Amazon and Microsoft tumbled. Here are some other notable premarket movers:

- Farfetch (FTCH US) shares fall as much as 4.43% in US premarket trading, after Citi begins coverage of the luxury online retailer with a sell rating, with broker flagging “weak” underlying profitability.

- Shares of US-listed Macau casinos jump in premarket trading, after Macau government said tour groups from mainland China could resume as early as November. Wynn Resorts (WYNN US) jumps 5.4%; Las Vegas Sands (LVS US) +6.9%, Melco (MLCO US) +9.6% and MGM resorts (MGM US) +1.6%

- Cryptocurrency-exposed stocks edged higher in premarket trading on Monday as Bitcoin rose above $19,000.

- Marathon Digital (MARA US) +1.9%, Coinbase (COIN US) +0.4%

- Keep an eye on Diana Shipping (DSX US) and Safe Bulkers (SB US) as Jefferies downgraded them to hold from buy and lowered dry bulk estimates to reflect the decline in dry bulk charter rates.

European shares extended their fall to Dec. 2020 lows; sliding 1% and extending losses as investors priced a major economic shock and recession. The Stoxx 600 Index was down 1% by 10:50am in London, touching its lowest since December 2020, with real estate and banks among the worst performing sectors, while technology shares outperformed. Italy’s FTSE MIB bucked broader European declines to trade little changed, after Giorgia Meloni won a clear majority in Sunday’s election, in line with expectations.

Easiest way to get your first Bitcoin (Ad)

Banks and real estate stocks were the worst-performing sectors in Europe on Monday, with declines led by UK stocks as the pound and UK bonds slump. The Stoxx 600 Banks Index and the Stoxx 600 Real Estate are both down at least 2.5% while the benchmark gauge is 1.1% lower. The bank index decline is led by UK names including Virgin Money (-10%), Lloyds (-4.6%) and NatWest (-4.5%). Virgin Money was today resumed with a hold rating at Berenberg; broker said that the lender is expected to see revenue declines and a sector- lagging return on tangible equity which will affect ability to re-rate. Among real estate stocks, the UK’s Safestore Holdings (-4.2%), Assura (-3.9%) and Derwent London (-3.8%) are among the worst performers; non-index member housebuilders, including Persimmon, Bellway and Taylor Wimpey, are also plunging as the pound’s slump prompts talk of emergency action by the Bank of England. Here are the most notable movers today:

- The Stoxx 600 Tech Index rises as much as 2.4%, set for its biggest one-day outperformance against the broader Stoxx 600 since early-August, with semiconductor stocks leading gains. Among chip stocks, ASML rose as much as +3.7% after Santander upgraded the stock to neutral from underperform

- Italy’s FTSE MIB index gains, bucking weaker markets in Europe, after Giorgia Meloni won a clear majority in Sunday’s election. While the outcome was in line with expectations, the fact that the coalition didn’t obtain a super majority needed to change the constitution reassures investors. Telecom Italia rose as much +7.4%, FinecoBank +5.1%, Moncler +4.4%

- Unilever shares rise as much as 3.7% after it announced that CEO Alan Jope will retire from the company at the end of 2023, in a move that Jefferies analyst Martin Deboo (buy) sees as a positive development.

- RPS Group shares rise as much as 13% after Tetra Tech’s agreed deal to buy the company at 222p/share in cash, representing a 7.8% premium to an offer WSP made in August. Liberum does not rule out a counterbid.

- Belimo shares rise as much as 8.5% since the market isn’t fully pricing in its growth outlook, Berenberg says in a note, moving to buy and establishing a Street-high CHF440 target. The stock gains as much as 8.1%, the most since March 2021.

- Zalando shares rise as much as 4.8% after Citi analyst says they like the long-term investment story, short-term earnings risks are still high.

- UK Domestics: the most remarkable reaction to Friday’s not-so-mini budget, however, might be in lenders’ shares. The decline in banking stocks reflects investors’ pessimistic view on Britain’s economy. HSBC fell as much as 2.9%; Lloyds -4.3%, NatWest -4.7% and Barclays -3.0%.

- Virgin Money UK shares drop as much as 10% after Berenberg resumed a hold rating in note, stating that in many ways the UK small banks are “more different than they are alike.”

- Utilities are the day’s worst-performing European sector. Citi analyst Piotr Dzieciolowski says the EU’s funding for its policy response has so far been insufficient and also expects uncertainty to persist for UK names. United Utilities fell as much as -3.4%, Drax -3.8%

Geopolitical risks from the war in Ukraine to escalating tensions over Taiwan and unrest in Iran also weighed on sentiment. Meanwhile, the OECD cut almost all growth forecasts for the Group of 20 next year while anticipating further interest-rate hikes, and a gauge of German business confidence deteriorated.

Earlier in the session, a rout in Asian stocks extended into Monday as rising concerns about a global recession and weak demand hit the region’s exporters and materials producers. The MSCI Asia Pacific Index declined as much as 2.3% to the lowest since April 2020, dragged lower by TSMC, BHP and Toyota Motor. All but one sector traded lower with materials leading the slump. South Korean stocks fell the most in the region, with the benchmark tumbling 3% to more than a two-year low. The Korean market’s heavy tech exposure has proven costly amid rising rates and a stronger dollar, with fears that a looming recession may wreak havoc on global demand. Gauges in Hong Kong and China reversed earlier gains as the region’s selloff intensified. Korea Assets Are Asia’s Biggest Losers on Global Recession Angst “Investor sentiment is again at the stage of extreme fear,” said Lee Kyoung-Min, an analyst at Daishin Investment. “It is becoming solid and clear that Kospi and other global stock markets are on a mid-to-long term downward trend.”

Asian stock benchmarks are being buffeted by global headwinds as well as risks of their own. The Federal Reserve’s relentless rate hike campaign is pushing Asian currencies lower and raising the risk of capital outflows, while China’s adherence to Covid Zero is hurting growth in the region’s economic giant. If Monday’s losses are extended through the week, the MSCI Asia Pacific Index will see its longest run of declines since 2015. Japan stocks declined more than 2% as the nation resumed trading after a holiday on Friday. The Philippine stock market was closed Monday as Super Typhoon Noru barreled into the main Luzon island. Among the key issues investors are watching this week are speeches by central bank officials in US and Europe, including Fed Chair Jerome Powell on Tuesday.

Japanese equities tumbled as the market reopened following a three-day weekend, tracking US peers lower after the Fed’s hawkish comments last week deepened fears of a global downturn. The Topix fell 2.7% to close at 1,864.28, while the Nikkei declined 2.7% to 26,431.55. Toyota Motor contributed the most to the Topix decline, decreasing 3.2% after its monthly production update lagged expectations. Out of 2,169 stocks in the index, 145 rose and 1,985 fell, while 39 were unchanged. “There is a possibility that inflation will not subside and interest rates will rise further, which the markets will not like,” said Shoji Hirakawa, a chief global strategist at Tokai Tokyo Research.

In Australia, the S&P/ASX 200 index fell 1.6% to close at 6,469.40, as energy and mining shares plummeted. An energy gauge including oil and coal linked securities declined by the most since March 2020. The New Zealand market was closed for a holiday

In India, key stocks gauges plunged to their lowest closing levels in almost two months as the global equity rout continues. The S&P BSE Sensex dropped 1.6% to 57,145.22 in Mumbai to its lowest since July 28. The NSE Nifty 50 Index fell 1.8%, its biggest single-day plunge since Sept. 16. Both the indexes, down in four of the past five weeks, have lost almost 6% since this month’s peak. Volatility in domestic equities is likely to remain elevated this week, pending monthly derivatives expiry on Thursday. Of 30 shares in the Sensex index, 24 fell and 6 advanced. All but one of the 19 sector sub-indexes compiled by BSE Ltd. declined, led by utilities and power companies. The Indian rupee weakened to a new record against the dollar amid surging US Treasury yields. The Reserve Bank of India’s rate-setting panel will announce monetary policy later this week.

As noted above, while stocks are ugly, rates are a horrorshow as Treasuries extended their worst bond slide in decades as a dollar gauge rose to yet another record. Treasuries extended losses in a bear flattening move with yields cheaper by up to 10bp across the belly of the curve. US 10-year yields around 3.78%, cheaper by 6bp on the day with 5s30s spread flatter by 5bp, dropping as low as -45.4bp in European session; UK yields cheaper by 60bp to 25bp from front- end out to long-end of the curve. The Move comes as market participants brace for accelerated policy tightening from global central banks and headlines such as this:

- *TRADERS PRICE IN UP TO 200BPS OF BOE RATE HIKES BY NOVEMBER

Yields on 2-year gilts are 60bp cheaper heading into early US session, while the pound recovers slightly after reaching a fresh all-time low. US session focus on 2-year auction, while a barrage of Fed speakers are expected for the week. Peripheral spreads widen to Germany with 10y BTP/Bund widening 7bps to 238bps.

FX, of course, is a disaster, with the Bloomberg Dollar Spot Index rising a fifth consecutive day as the greenback advanced versus most of its Group-of-10 peers.

- The pound plunged almost 5% to $1.0350 in Asian trading, the lowest recorded in Bloomberg data going back to 1971, while gilts crashed after the UK government vowed to press ahead with more tax cuts, stoking fears that new fiscal policies will send inflation and debt soaring, triggering emergency rate hikes. The options market signals no respite even as the pound rebounded from a record low hit during the Asia session. The yield on two- year bonds surged more than 55 basis points to 4.51%, while the 10-year yield rose 37 basis points to 4.19%. Money markets price in more than 150 basis points of rate increases by the BoE’s next policy meeting in November

- The euro steadied after earlier dropping to $0.9554; European bond yields rose; Italian bonds underperformed German peers. Giorgia Meloni won a clear majority in Sunday’s Italian election, setting herself up to become the country’s first female prime minister at the head of the most right-wing government since World War II. Germany’s IFO business expectations slid to 75.2 in September from 80.3 in August. That’s the lowest since April 2020. Analysts had predicted a drop to 79. An index of current conditions also fell.

- The Australian and New Zealand dollars pared some losses after earlier touching fresh 2-year lows. Aussie bond yields rose by up to 13bps, led by the front end

- The yen weakened amid a broadly stronger dollar. Bank of Japan Governor Haruhiko Kuroda said the government’s intervention in the foreign exchange market last week was appropriate given the recent volatility in the yen

The currency’s rally is “untenable” for risk assets, according to a note by Morgan Stanley strategists led by Michael Wilson, while Sian Fenner, senior Asia economist for Oxford Economics, said that “It’s a king US dollar…“It’s adding to inflationary pressures and more central banks raising rates more than we have historically seen.”

In commodities, WTI slides almost 1% to trade near $78/bbl. Spot gold mostly unchanged near $1,643/oz. Bitcoin climbs above $19,000.

Trading this week will be punctuated by a number of economic reports including US initial jobless claims and gross-domestic-product data, along with PMI figures from China. Choppiness in price moves is likely with a steady stream of Federal Reserve officials speaking through the week.

Looking at today’s calendar, we get the September Dallas Fed manufacturing activity index, and the August Chicago Fed national activity index. Central bank speakers include the Fed’s Bostic, Collins, Logan and Mester; ECB’s Lagarde also speaks as does Nagel, Guindos, Centeno and Panetta speak, BoE’s Tenreyro speaks.

Market Snapshot

- S&P 500 futures little changed at 3,706.25

- MXAP down 2.0% to 142.24

- MXAPJ down 1.4% to 463.08

- Nikkei down 2.7% to 26,431.55

- Topix down 2.7% to 1,864.28

- Hang Seng Index down 0.4% to 17,855.14

- Shanghai Composite down 1.2% to 3,051.23

- Sensex down 1.2% to 57,378.30

- Australia S&P/ASX 200 down 1.6% to 6,469.41

- Kospi down 3.0% to 2,220.94

- STOXX Europe 600 down 0.2% to 389.70

- German 10Y yield little changed at 2.08%

- Euro little changed at $0.9683

- Brent Futures down 0.7% to $85.59/bbl

- Brent Futures down 0.7% to $85.59/bbl

- Gold spot up 0.1% to $1,645.98

- U.S. Dollar Index little changed at 113.22

Top Overnight News from Bloomberg

- Chancellor of the Exchequer Kwasi Kwarteng must do more to reassure the markets about his plans for the economy after a selloff sent the pound crashing to an all-time low against the dollar, said Gerard Lyons, an external adviser to Prime Minister Liz Truss

- The UK’s foreign currency holdings are a fraction of the huge stockpiles built up by some of its peers, making unilateral intervention in the market to prop up the plunging pound a tall order for UK policymakers. The UK had $108 billion in foreign currency reserves at the end of August, according to data from the IMF

- Hedge funds ramped up bullish bets on the pound just days before the UK government’s unexpectedly large tax cuts sent the currency tumbling

- The ECB’s newest policy maker, Boris Vujcic, says “it’s clear that this is the right way to go,” backing this month’s 75-basis point interest-rate hike

- ECB Vice President Luis de Guindos said the biggest problem facing the continent’s economy is record inflation, which is becoming more broad-based, threatening investment and consumer spending

- ECB Governing Council member Yannis Stournaras says the central bank must maintain the main principles of gradualism and flexibility, since the problem it faces is different from the one that the US Fed faces

- China made it more expensive to bet against the yuan in the derivatives market, ramping up support for the currency as it slides toward the weakest level since the 2008 financial crisis

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks traded mostly negative in a resumption of last week’s global stock rout amid the continued surge in the dollar and higher yields, while there was also FX volatility which saw a flash crash in GBP/USD to a record low. ASX 200 was dragged lower amid losses in the commodity-related sectors and with sentiment dampened by the collapse of potential M&A deals involving Ramsay Health-KKR and Link Administration-Dye & Durham. Nikkei 225 underperformed with Mazda Motors among the worst hit as it considers exiting Russian operations. Hang Seng and Shanghai Comp retraced most of their initial losses with Hong Kong underpinned following the scrapping of hotel quarantine policy and with casinos boosted as Macau is to resume tour groups from China, while the property industry benefits after China Construction Bank formed a CNY 30bln housing rental fund and some Twitter sources also circulated that some China state banks were reportedly ordered to buy stocks to contain selling.

Top Asian News

- PBoC injected CNY 42bln via 7-day reverse repos with the rate kept at 2.00% and CNY 93bln via 14-day reverse repos with the rate kept at 2.15% for a net CNY 133bln injection.

- There were rumours circulating on social media of a coup against Chinese President Xi, although experts and journalists in Beijing dismissed the rumours and said there was no evidence to support them, according to The Print.

- Philippines Stock Exchange announced a trading suspension for Monday amid a typhoon in the capital, according to Reuters.

European bourses are softer after a mixed cash open and despite a brief foray higher, Euro Stoxx 50 -0.5%, as sentiment remains subdued amid recession/inflation concerns. The breakdown features modest outperformance in the FTSE MIB as Italian election results are in-line with expectations. Stateside, futures are lower across the board in-fitting with peers going into a week of Fed speak and inflation data.

Top European News

- UK PM Truss said she is determined to make the special relationship with the US even more special and said she agreed with US President Biden that it is vital to protect the Northern Ireland Good Friday Agreement, while she wants to find a way forward with a negotiated solution with the EU, according to Reuters and a CNN interview.

- UK PM Truss is to review visa schemes in an attempt to ease UK labour shortages, according to FT.

- UK Chancellor Kwarteng hinted that more tax cuts are on the way and claimed his tax cuts “favour people right across the income scale” amid accusations they mainly help the rich, according to Evening Standard.

- UK Chancellor Kwarteng said he is focused on growing the economy and the longer term when asked about the market reaction to his statement on Friday. Kwarteng added that he shares ideas with BoE Governor Bailey but added that Bailey is completely independent and Kwarteng is confident the BoE is dealing with inflation, according to Reuters.

- UK opposition Labour Party leader Starmer said they would reintroduce the top rate of income tax at 45% which the government announced to scrap last week, while he added that they will support the government plan to lower the basic rate of income tax to 19%, according to Reuters.

- Italy’s right-wing bloc is seen winning the national election with 43.3% and centre-left bloc is seen winning 25.4%, according to the first projection by LA7 TV based on the actual vote count.. Click here for newsquawk snap analysis.

- Italy’s Meloni said Italians gave clear backing to a centre-right government led by the Brothers of Italy and said the situation is difficult and needs contribution from everyone. It was separately reported that Italy’s Democratic Party conceded in the election and said it will be the main opposition force, while Italy’s Meloni claimed leadership of the next Italian government, according to Reuters and AFP.

FX

- DXY climbed to a fresh YTD high of 114.58 before paring modestly, but remaining firmer, as GBP in particular lifts off worst levels.

- Cable succumbed to a flash crash overnight, with GBP/USD hitting an all-time-low around 1.0350 as participants confidence in the economy slips.

- EUR suffers amid the mentioned USD move but derives relative benefit from GBP, while ECB speakers thus far have added little.

- Antipodeans and CAD weighed on by broader risk and commodity pressure.

- Japanese Finance Minister Suzuki said the government and BoJ share views on concerns about a weak JPY, while he added that FX intervention had a certain effect and there is no change to the stance that they will respond to market moves as needed, according to Reuters.

- PBoC set USD/CNY mid-point at 7.0298 vs exp. 7.0019 (prev. 6.9920)

- PBoC imposed a 20% risk reserve requirement for FX forward sales from September 28th to rein in yuan weakness.

Fixed Income

- Gilts have retained some composure after slumping over 200ticks at the commencement of trade and have settled around halfway between intraday extremes.

- EGBs downbeat in sympathy while BTPs marginally lag core-EGB peers as Italian as-expected election results are digested with BTP-Bund only modestly wider as such.

- Stateside, USTs are pressured in-fitting with peers and also conscious of the week’s supply docket getting underway via a 43bln 2yr.

Central Banks

- Fed’s Bostic (2024 voter) said inflation is too high and that they need to do all they can to bring it down and said demand is beginning to shrink which will ultimately pay dividends in inflation levels. Bostic also stated that there are scenarios where they can avoid deep pain but there will likely be some job losses, according to Reuters.

- BoJ’s Kuroda says the BoJ will maintain accommodative monetary conditions to support companies, hopes to support a positive economic cycle, long-term inflation expectations have begun to heighten, via Reuters. Intervention from the MoF is an “appropriate” move, does not think gov’t intervention and BoJ policy are contradictory. Amamiya says the domestic economy is picking up, must carefully watch how FX moves affect the economy and prices.

- BoJ Governor Kuroda says when he stated that BoJ forward guidance will not change for 2-3yrs, did not refer to guidance on keeping short and long-term rates at present of lower levels via Reuters.

- ECB’s de Guindos says Q3 and Q4 point towards growth rates being close to zero within the EZ, the scenario is market by high uncertainty, lower growth and higher inflation.

- ECB’s Panetta says ECB is assessing the potential of distributed ledger technology (DLT) and “the extent to which it could improve our services.”.

- Capital Economics calls for the BoE to “get on the front foot with a big rate hike”. Allianz’s El-Erian says, on GBP, the fall is about extra tax cuts and Chancellor Kwarteng could recalibrate this. Alternative, would be for the BoE to hike at an emergency meeting. Adding, he would hike by 100bp.

- BoE publishes key elements of the 2022 annual cyclical scenario stress test; includes a scenario where the Bank Rate is assumed to rise rapidly to a peak of 6% in early 2023 before gradually reduced to sub-3.5%.

Commodities

- WTI and Brent November futures remain subdued in early European trade following last week’s recession-induced losses.

- Spot gold trades in tandem with the Buck and sees resistance at around USD 1,650/oz after falling to USD 1,627/oz as a casualty of the Sterling flash crash overnight.

- LME metals are softer across the board with 3M copper futures having a hard time reclaiming USD +7,500/t status with upside capped by the Buck.

- Iraq began trial operations at the Karabala oil refinery which has a production capacity of 140k bpd, according to a statement from the Oil Ministry.

- German Chancellor Scholz signed a strategic agreement with UAE’s President on accelerating energy security and industrial growth, while UAE’s ADNOC signed an agreement with Germany’s RWE which includes ADNOC exporting its first LNG cargo to RWE and will conduct trial shipments of low-carbon ammonia to Germany. Furthermore, Chancellor Scholz said while visiting Doha that he talked with the Emir about LNG deliveries and that they want to achieve further progress, according to Reuters.

- Germany is preparing a national electricity price cap to be implemented this fall in the scenario the EU falls to agree on a similar move for the entirety of the bloc, via WSJ citing officials.

- Vitol’s CEO said at the Asia Pacific Petroleum Conference that Russian gas supply cuts put enormous strain on supply-demand in Europe and that high gas prices are to impact 60%-80% of demand, while Ecopetrol’s CEO said they are increasing crude exports to Europe this year to replace Russian supplies and are drilling 600 oil wells this year.

- Anglo American (AAL LN) tightens copper production guidance for Chile to 560k-580k tonnes of copper (prev. 560k-600k tonnes) due to lower throughput at Los Bronces caused by a combination of water restrictions and a change in ore characteristics, via Reuters.

US Event Calendar

- 08:30: Aug. Chicago Fed Nat Activity Index, est. 0.23, prior 0.27

- 10:30: Sept. Dallas Fed Manf. Activity, est. -10.0, prior -12.9

Central Banks

- 10:00: Boston Fed’s Susan Collins Speaks to Boston Chamber of…

- 12:00: Fed’s Bostic Discusses Income Inequality

- 12:30: Fed’s Logan Speaks at Banking Conference

- 16:00: Fed’s Mester Discusses Economic Outlook

DB’s Jim Reid concludes the overnight wrap

I wonder whether any research report has ever been written whilst watching synchronised swimming? Well if not, then you’re reading the first ever as I’m getting a head start on the early morning news by starting this on Sunday evening watching my daughter Maisie do her second session after getting into the local club. Watching this sport is going to take some getting used to after years of watching football, cricket, golf, F1, athletics, rugby… actually…. virtually every sport bar synchronised swimming.

I think everyone felt they were swimming in a tsunami of newsflow last week after one of the most incredible macro weeks in recent memory in terms of breadth of events. Yes there have been more extreme weeks in crises but last week had a bit more variety and was outside of a crisis period. If over 500bps of global rate hikes wasn’t enough, you also had 2yr US yields moving higher for the 12th successive day on Friday (the longest steak since data begins in 1976), the BoJ intervening in FX markets for the first time since 1998, and what can only be termed as one of the darker days for sterling assets on record on Friday after a mammoth tax giveaway in what was a mini-budget in name and not by nature.

Henry and I put a note out on Friday night (link here) showing that it was the third worst day for Sterling (-3.57%) since Black Wednesday in 1992, with the worst two since being the day after the Brexit vote (-8.1%) and after the initial covid shock in 2020 (-3.71%) when there was a global flight to dollars. We also show a graph of daily Sterling moves back to 1862 and on that it was the 41st worst day in history spanning 47,000 trading days. Obviously in the long era of fixed FX rates there were the occasional big devaluations which were much bigger than Friday. This morning is Asia it fell around -4.5% at one point (1.0392) which was a record low against the Dollar. It’s around -2.78% as I type. This follows a weekend interview where Chancellor Kwarteng suggested that more tax cuts were to come so that certainly was a red rag to markets. Will we hear from the upper echelons of the BoE today? Watch out for any comments, especially at the market open. DB’s George Saravelos suggested on Friday that the Bank of England need to do an inter meeting hike to restore policy credibility.

There’s also a graph in our note mentioned above showing that Friday was the worst day for 5yr gilts (+50.3bps) since a +200bps hike in 1985 when sterling was also slumping. So maybe omens here.

I suppose the only slight mystery is the timing of the sell-off as the mini-budget in magnitude was broadly in-line with the recent elevated fiscal expectations that had been building. However perhaps it was the unabashed revival of trickle-down economics that had markets a little aghast. It goes against the current economic orthodoxy and the overall zeitgeist of our immediate times. As such there is likely to be concerns of a credibility issue.

We are publishing our long-term study today with the title “How we got here, and where we’re going?”. In it we try to put the current macro woes into historical context in an attempt to work out where we’re going. There are quite a few people who have proof-read it on my team and they were all thoroughly depressed at the end. I didn’t feel that way writing it but maybe it’s a case of starting point perceptions. Anyway, look out for it around the European lunchtime.

Overnight in Italy, the right-wing alliance led by Giorgia Meloni’s Brothers of Italy party was on course to become the nation’s first woman prime minister after exit polls gave it a clear majority. With the full results due later today, she is predicted to win up to 26% of the vote ahead of her closest rival Enrico Letta from the centre left. The right wing alliance is slated to be on course for around 43% of the vote, enough for a majority if correct. As I type, the euro is extending its losses against the dollar for the fifth day, its longest streak since April 28, falling as much as -0.5% to 0.9638, albeit being overshadowed by Sterling.

For this week we have an array of consumer-driven economic data in the US and some important European inflation prints. We will also get a number of consumer sentiment indicators across the key economies and PMIs from Asia. Away from the data, there are more than 30 central banker appearances across the Fed and the ECB to keep markets busy. Tomorrow also sees referendums in the Russia-annexed Ukrainian territories as the conflict goes into its eight month.

Going through the data in more details now. Starting with the US, the PCE and personal income and spending data will be front and centre for markets next week as they gauge the extent of inflationary pressures and the strength of the consumer. The Fed’s preferred inflation gauge, the PCE, due Friday, will be watched for signs of price pressures we saw in last week’s CPI report. Our US economists expect core PCE to edge higher by +0.5% MoM (vs +0.1% in July) which won’t allow the Fed to take the foot off the tightening pedal. For the other two data points, our team forecasts a +0.1% MoM increase for both income and consumption. Final US Q2 GDP will also be released on Thursday and although DB expect no change to the -0.6% second reading, watch out for the annual benchmark revisions back to Q1 2017. History could be re-written that could have some implications for how we all think about the economy. In other US data, we will also get the consumer confidence index on Tuesday, along with durable goods orders, and inventories data on Wednesday, with the Chicago PMI on Friday.

Over in Europe, all eyes will be on September’s inflation data, including the Euro Area flash CPI release on Friday. Our economists are expecting the measure to hit a record +9.5%, up from the previous record of +9.1% in August. Other data in the region will include consumer and economic sentiment from Germany, France, Italy and the Eurozone throughout the week. Meanwhile, EU energy ministers will meet again on Friday regarding the emergency intervention amid elevated energy prices.

Finally, next week’s earnings line up will feature a number of retail bellwethers on Thursday. Among them will be Nike, H&M and Next. Micron will report that day as well. See our usual day by day guide to the week at the end which contains many of the key Fed and ECB speakers including Powell and Lagarde.

Stock markets across Asia are mostly lower this morning. The Kospi (-2.40%), Nikkei (-2.30%) and the S&P/ASX 200 (-1.40%) are leading the declines. Meanwhile, the Hang Seng (+0.11%) is swinging between gains and losses after rising by +2.45% initially with Chinese shares mixed as the Shanghai Composite (-0.10%) is trading lower while the CSI (+0.46%) is up as we go to press. Stock futures in DMs are pointing to further losses with contracts on the S&P 500 (-0.49%), NASDAQ 100 (-0.46%) and DAX (-0.33%) all moving lower.

Early morning data showed that Japan’s manufacturing sector continued to expand albeit at a slower pace as the latest au Jibun Bank manufacturing PMI slipped to a 20-month low of 51.0 in September from 51.5 in August, pulled lower by high energy and raw material prices that was exacerbated by a weak yen. At the same time, the au Jibun Bank services PMI returned to expansion, recording a level of 51.9 in September from August’s 49.5 final reading.

Moving on to China, in order to stabilise expectations in the FX market, the People’s Bank of China (PBOC) today raised the risk reserve requirement on foreign exchange forward sales to 20% from 0% beginning September 28 as the yuan faces increasing depreciation pressure, in line with most major currencies amid broad dollar strength.

Looking back now on a week that will not be forgotten anytime soon. While there were historic central bank hikes all week, the biggest news came from the fiscal authorities, following the UK’s budget Friday, which had the largest tax cut package since the 1970s.

Gilt yields had their largest one-day increase in decades with 2yrs +44.7bps, 5yrs +50.3bps, and 10yrs +33.3bps. As we mentioned at the top, 5yrs yields saw their largest move since 1985 after a +200bps hike aimed at helping a plunging currency. The pound fell -3.57% against the US dollar to within a percentage point of the weakest in the post-Bretton Woods 51yr free float era.

It was already a busy macro week before the blockbuster budget, where we got more than 500bps of global central bank hikes and a currency intervention from Japan. In terms of the biggest players, the Fed delivered its third consecutive 75bp hike while the BoE delivered its second 50bp hike in a row, with both banks guiding toward yet more tightening, while the BoJ remained the outlier by keeping its accommodative policy in place, which isn’t going to help the yen turnaround even with intervention.

When all was said and done, sovereign bonds and equities sold off in size, while yield curves flattened. 2yr Treasuries (+33.4bps, +7.9bps Friday), 2yr Bunds (+38.5bps, +7.2bps Friday), 2yr Gilts (+82.1bps, +44.7bps Friday) reached their highest levels since 2007, 2008, and 2008, respectively, as markets priced in more tightening to overcome inflationary pressures (and in the case of the UK, fiscal expansion). 10yr Treasuries (+23.5bps, -2.9bps Friday) ended the week a touch lower on the day but hit their highest levels since 2011 during the week, while 10yr Bunds (+26.8bps, +5.9bps Friday), and 10yr Gilts (+69.1bps, +33.3bps Friday) hit their highest levels since 2013 and 2011, respectively.

The mixture unsurprisingly proved unpalatable to risk assets, driving the STOXX 600 and S&P 500 back to their lows for the year. The STOXX 600 retreated -4.37% on the week and -2.34% on Friday, the worst weekly and daily return since mid-June. The S&P 500 fell -4.65% (-1.75% Friday), returning to bear market territory. The FTSE managed to stay above its YTD lows, but still fell -3.01% on the week, its worst weekly return since mid-June as well, and retreated -1.97% on Friday, the worst daily return since early July.

Source: ZeroHedge

Top image: Pixabay

Become a Patron!

Or support us at SubscribeStar

Donate cryptocurrency HERE

Subscribe to Activist Post for truth, peace, and freedom news. Follow us on SoMee, Telegram, HIVE, Flote, Minds, MeWe, Twitter, Gab, What Really Happened and GETTR.

Provide, Protect and Profit from what’s coming! Get a free issue of Counter Markets today.

Be the first to comment on "“Global Gloom”: World Markets Plunge To Start The Week As Global Currency Crash Hits Max Pain And Beyond"