By Tyler Durden

By Tyler Durden

As we discussed yesterday, when looking at the recent dip in sky-high container shipping rates, there was some fleeting hope that Southern California port congestion had turned the corner. The number of container ships waiting offshore dipped to the low 60s and high 50s from a record high of 73 on Sept. 19, trans-Pacific spot rates plateaued, the Biden administration unveiled aspirations for 24/7 port ops, and electricity shortages curbed Chinese factory output.

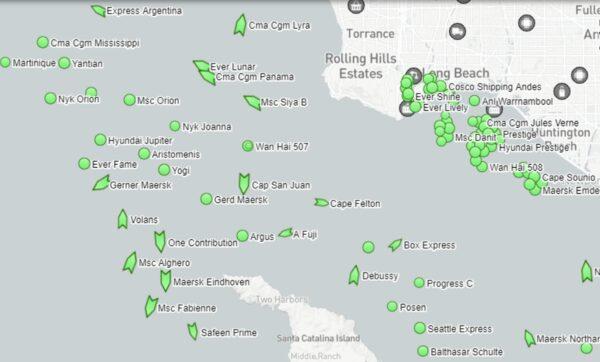

Alas, it was not meant to be, and despite the very serious jawboning coming out of the White House, the time that ships are stuck waiting offshore continues to lengthen. There are simply too many vessels arriving with too much cargo for terminals, trucks, trains and warehouses to handle, and according to the Marine Exchange of Southern California, 79 container ships were waiting off Los Angeles and Long Beach on Thursday, yet another all-time record.

In light of this record parking lot that has formed outside of LA…

Map: Marine Traffic

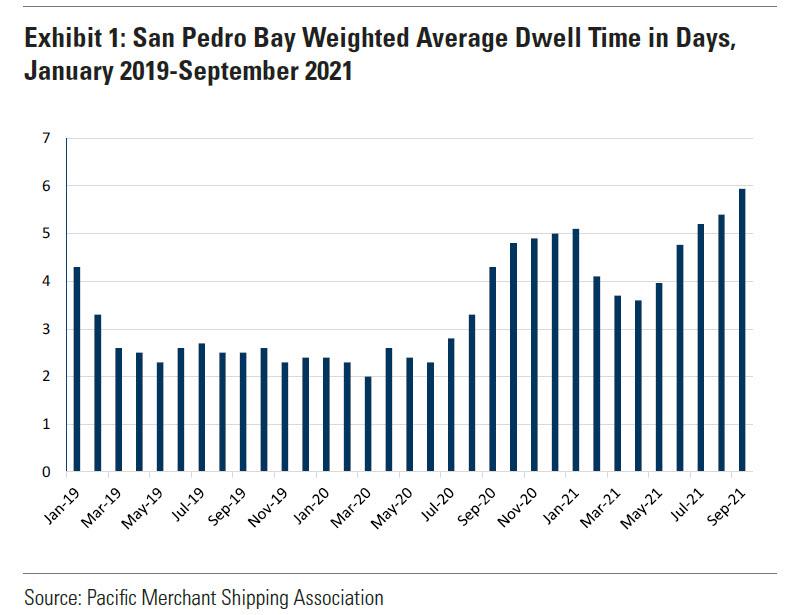

… it is hardly a surprise that container dwell times have steadily increased over the summer and now into the fall, increasing to an average of 5.9 days in September – up nearly 2.5 days since the April low of 3.6 days, according to Goldman Sachs.

Food Storage Feast – Online Cooking Course for Long Term Storage Foods (Ad)

Goldman also notes that the proportion of containers that have been dwelling for longer than five days were 32.8% of total containers in September – up from 13.1% in the spring and 21.2% in September 2020 when dwell time began to accelerate as consumer demand returned.

While it is obvious, it is important to note that higher dwell times at the ports and terminals lead to less overall supply chain efficiency and can impact volume throughput. For example, JBHT recently reported during their 3Q21 earnings call that congestion led to lower container turn efficiency to 1.62 from the end of 2Q21.

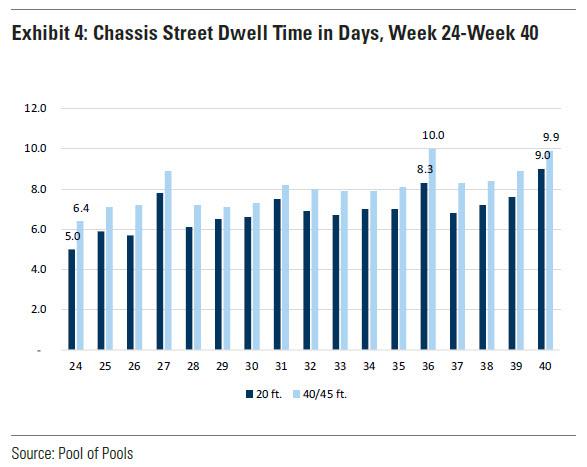

Chassis also saw accelerated street dwell times in the most recent week (week 40) in the Port of L.A. and Long Beach. August (Weeks 37-39) averaged a street dwell time of 7 days before increasing to 9.0 days in Week 40 for 20 ft. chassis. 40/45 ft. chassis similarly jumped in mid-October to 10 days from the 8.5 day average over the previous three weeks.

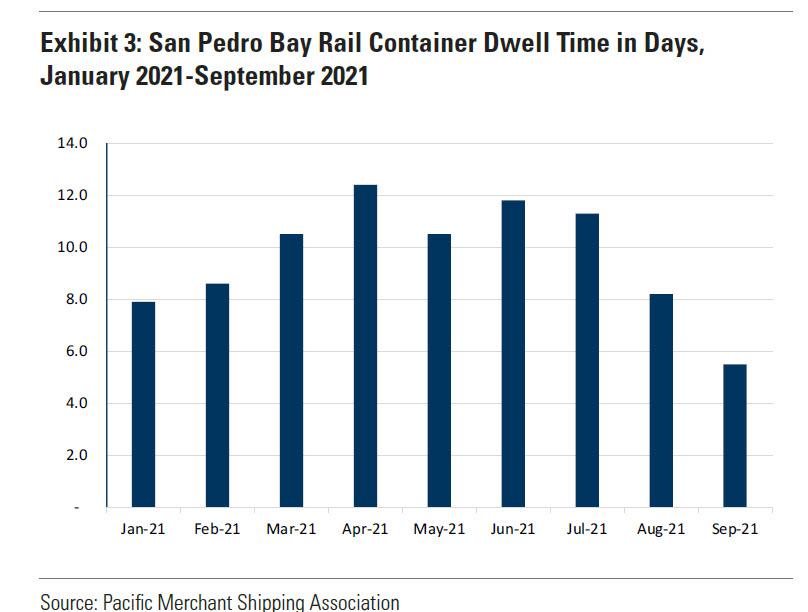

It’s not all bad news: in recent weeks, rails have seen an opposite trend as fluidity has continued to improve in their networks starting at the ports, decreasing their average dwell time to 5.5 days in September from 11.8 day high in June.

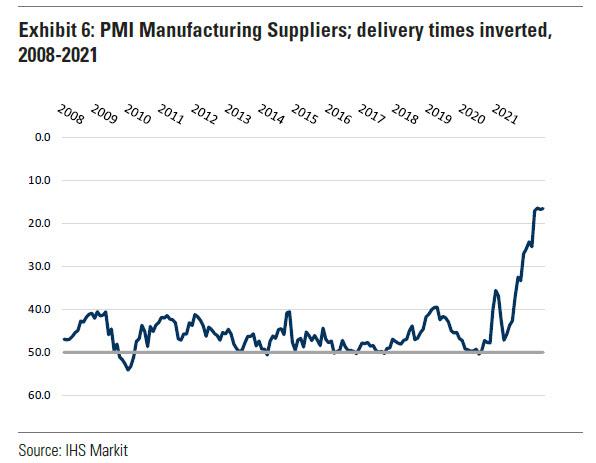

As a result of the surge in client interest in supply chain issues on the West Coast, Goldman recently introduced the PMI Manufacturing Suppliers’ delivery times index from IHS Markit to its supply chain congestion tracker. Purchasing managers respond to IHS Markit’s PMI surveys indicating if it is taking their suppliers more or less time to provide inputs to their manufacturing. Above 50 indicates that supply delivery times are faster and below indicates that delivery is slower. Manufacturers have reported significant increases in delivery times, with the current index level in September at 16.6 – down significantly from July 2020 of 47.2.

On an inverted basis, the index has increased 62% YoY in September reflecting the large increase in supplier delays.

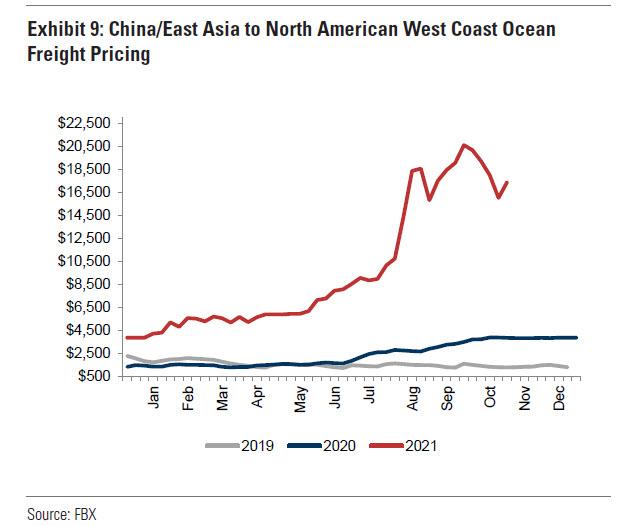

On a roll, Goldman then makes another patently obvious observation, noting that congestion at the ports ultimately leads to higher rates in ocean freight, and it can also have an impact to air and truck rates as well.

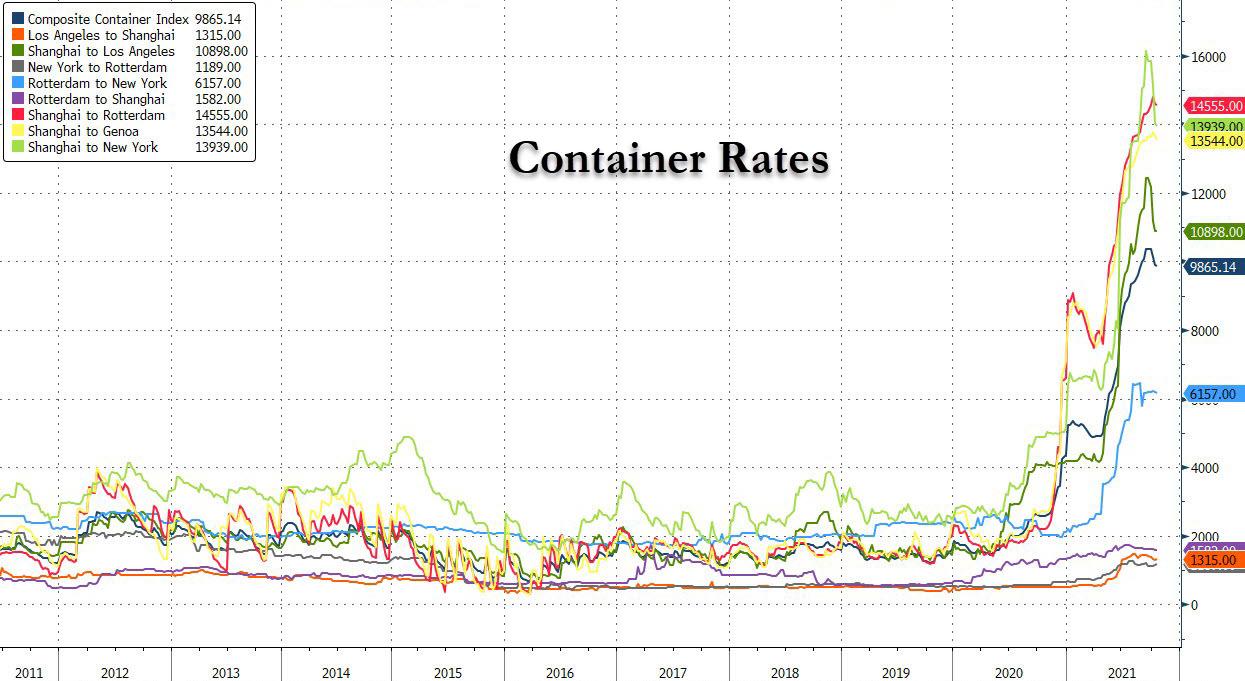

To be sure, as noted above, while prices have started to abate from record levels in mid-September in ocean freight (don’t get your hopes up – this is entirely due to another temporary lockdown in Chinese supply chains, a result of the reduction in manufacturing due to China’s ongoing power crunch and energy crisis), they still increased +350% YoY in the week ending October 15. Prices will remain elevated until congestion abates or demand normalizes; it is unclear when either of these will happen.

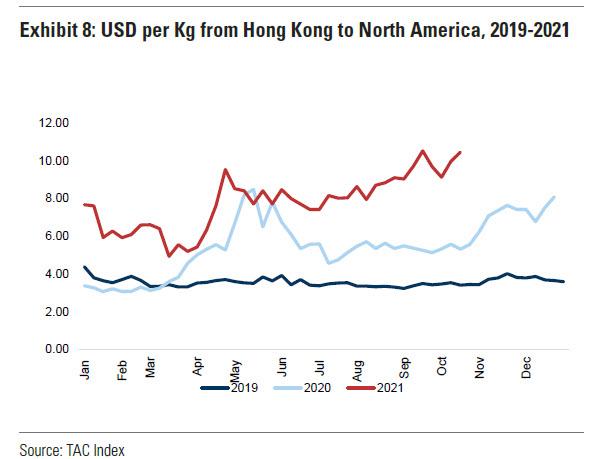

More ominously, as of October 18, airfreight from Hong Kong to North America was $10.45 per Kg, up +97% YoY from $5.31.

Goldman’s bottom line is that the data the bank tracks for supply chain congestion lines up with company commentaries during conferences in August and at the start of this current 3Q21 earnings season. In the short term, the bank continues to expect the increase in congestion to benefit asset light and freight forwarders from increased rates and the need to facilitate moves that asset based providers do not have the capacity to handle (translation: it will negatively impact everyone else who is reliant on Just In Time supply chains). Moreover, overall supply chain tightness should help keep truckload rates elevated, and the parcel sector could see ongoing benefit from shippers forced to use air capacity if unable to gain ocean container capacity.

Of course, this being Goldman, the bank has to end on a positive note, and in its forecast writes that while ports reflect congestion in the short term, “we do expect some slight easing as we pass peak season shipping in late October for the holiday season and more abatement as we pass Chinese New Year in early 2022.” The bank also expects the abatement in congestion to positively benefit the rails as well as intermodal participants (such as JB Hunt) as fluidity improves and congestion related costs and service issues begin to abate.

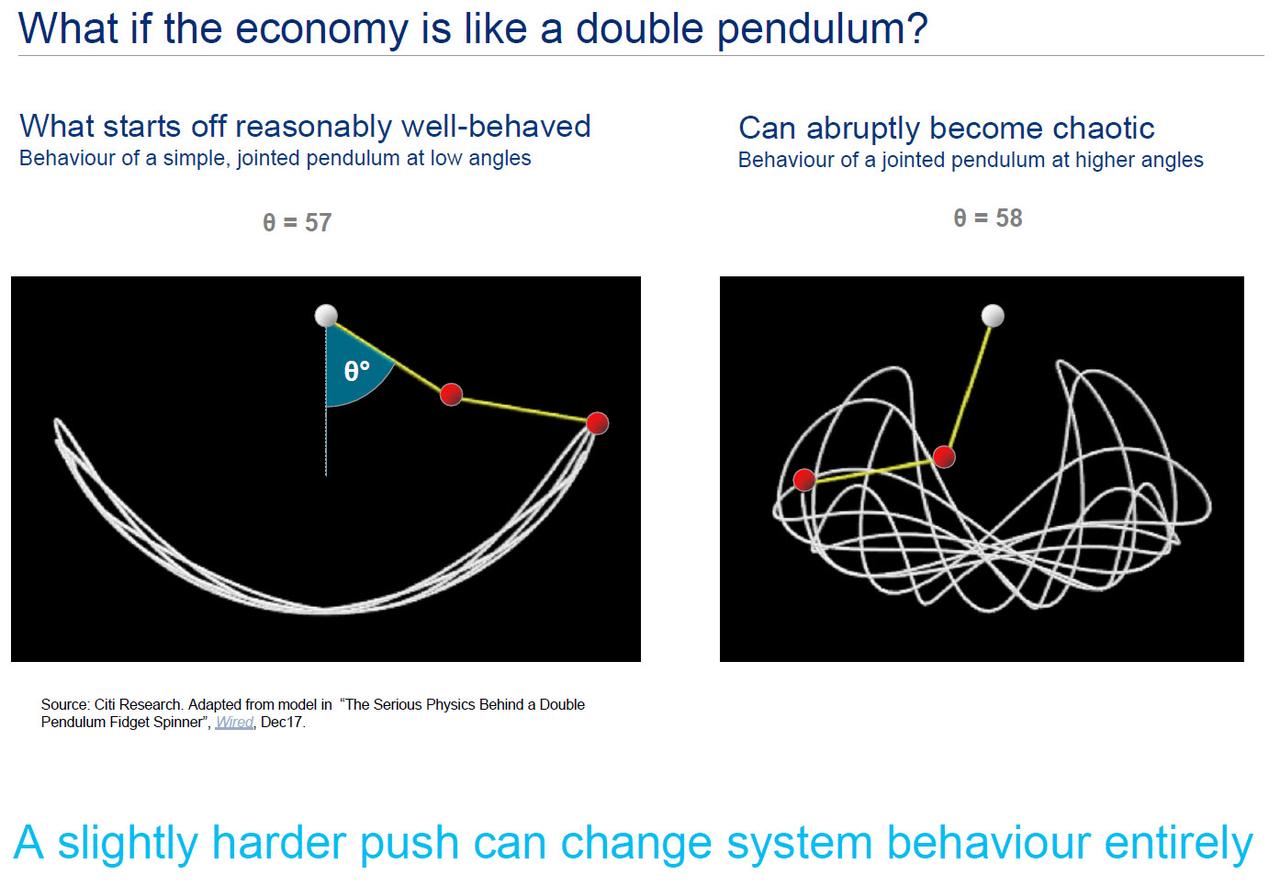

Alas, unlike Goldman, we don’t see any easing in the short- to medium-term, for several reasons. First, there is no catalyst on the horizon that will lead to both a reduction in demand for goods (over services) over the next 6 months especially with winter coming. Second, the downstream chaos in the supply chain alone means that everything has to align perfectly for the blockages to be resolved. However, that won’t happen because between the continued labor shortages, the lack of infrastructure to resume smooth operations, and a supply pipeline that it snarled on both ends (Chinese energy crisis, US labor crisis), the chaos will continue indefinitely. This is a key point made recently by Citi’s Matt King in his latest must read presentation (available to pro subs), asking if the economy is like a “double pendulum” where a “slightly harder push changes the system behavior entirely.”

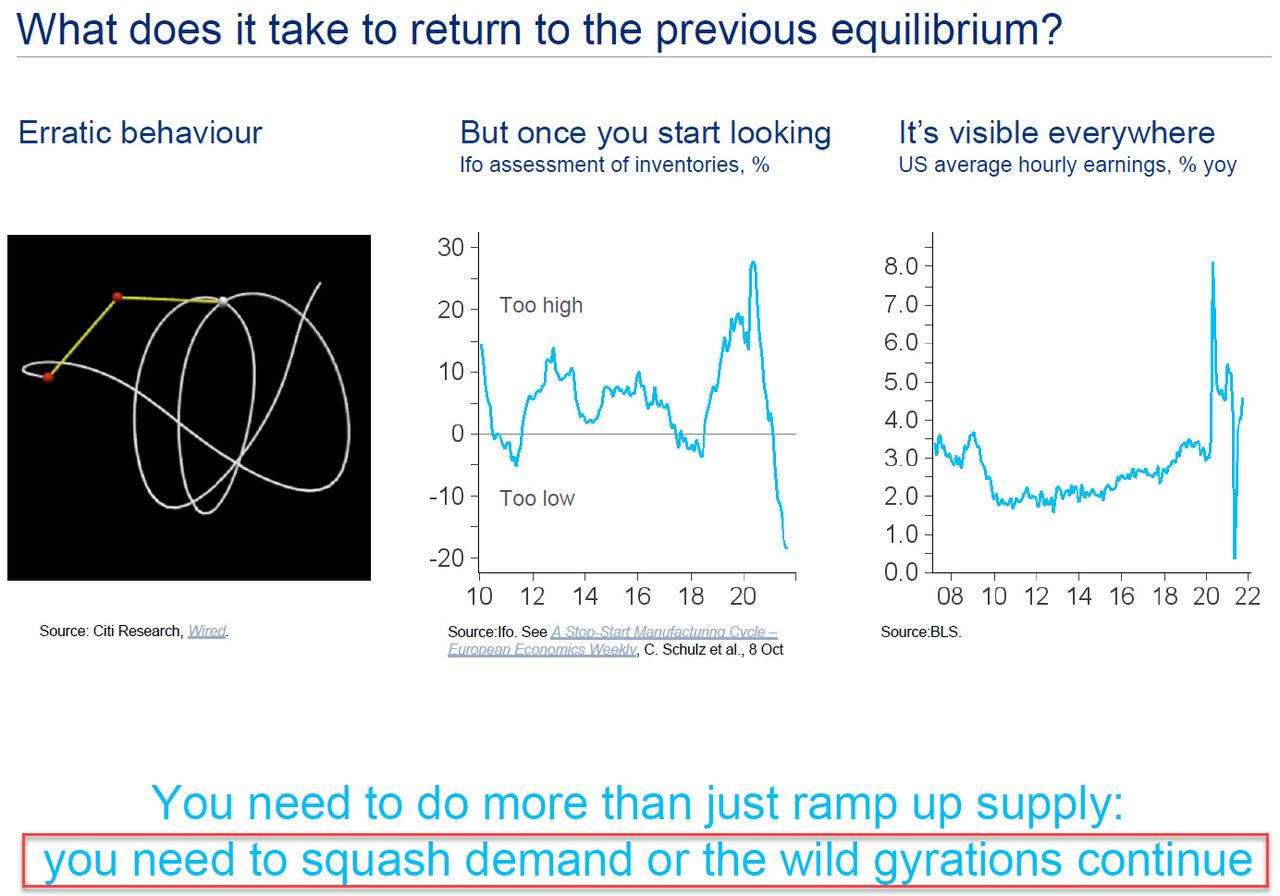

It gets worse though: so far the supply chain bottlenecks have not materialized in any tangible shortages at the retail level where rising prices have successfully offset rising demand (with a few notable exceptions). However, if and when the supply crisis hits a tipping point and photos of empty shelves once again flood the media, there will be a surge to hoard similar to what we saw in March 2020 as the panicked population buys first and asks questions later, at which point the chaos in the system will once again spill over. Or, as King puts it, “the desire to buy is inversely proportional to the stock available.”

Which leaves us with the painful conclusion: if we want a return to the previous supply-chain equilibrium, the system needs to do more than just ramp up supply: it also needs to squash demand or the wild gyrations will continue.

That means inducing another artificial recession to cripple demand, something which we doubt the Democrats controlling the 78-year-old in the White House will be able to stomach.

Source: ZeroHedge

Become a Patron!

Or support us at SubscribeStar

Donate cryptocurrency HERE

Subscribe to Activist Post for truth, peace, and freedom news. Follow us on Telegram, HIVE, Flote, Minds, MeWe, Twitter, Gab and What Really Happened.

Provide, Protect and Profit from what’s coming! Get a free issue of Counter Markets today.

Be the first to comment on "With A Record 79 Container Ships Waiting Off The SoCal Coast, A Scary Supply-Chain Solution Emerges"