By Tyler Durden

By Tyler Durden

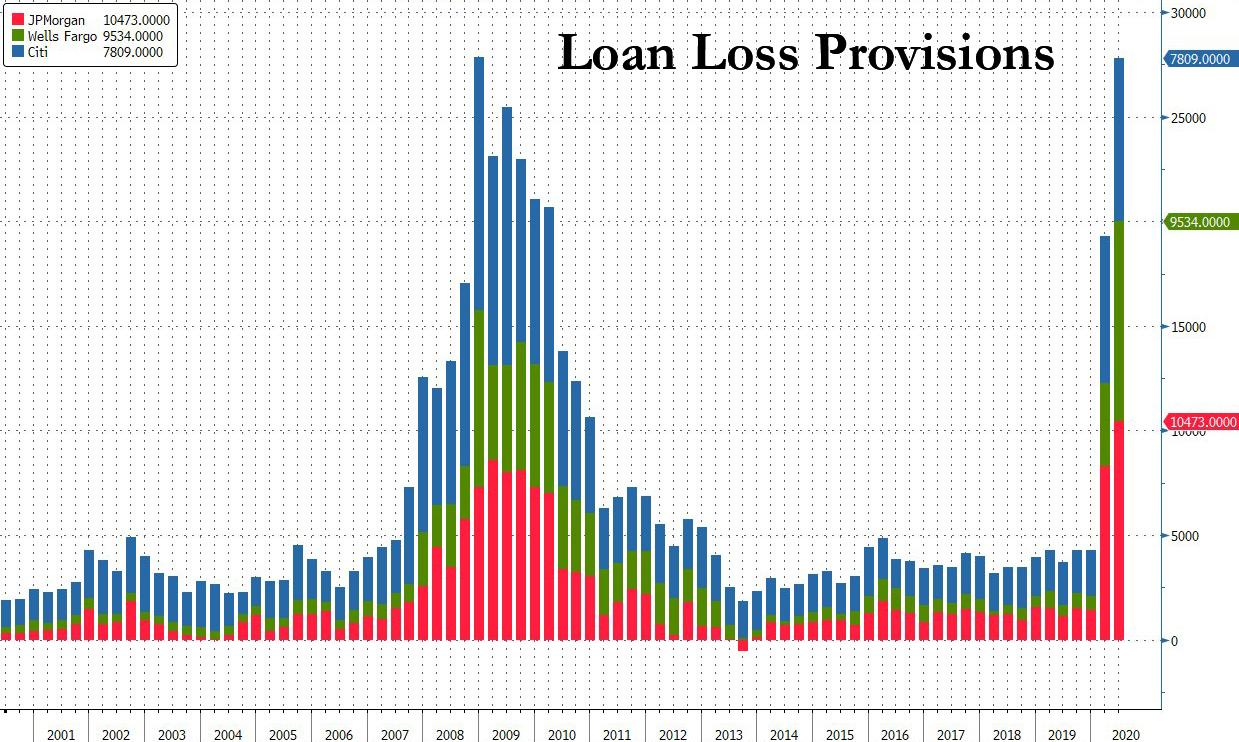

One quarter ago we pointed out something concerning: shortly after JPMorgan reported that its loan loss provision surged five-fold to over $8.2 billion for the first quarter, the biggest quarterly increase since the financial crisis, in preparation for the biggest wave of commercial loan defaults since the financial crisis (a number which in the latest quarter surged to $10.5 billion along with all other banks’ loan loss provisions)…

… the bank hinted that things are about to get much worse when it first halted all non-Paycheck Protection Program based loan issuance for the foreseeable future (i.e., all non-government guaranteed loans) because as we said “the only reason why JPMorgan would “temporarily suspend” all non-government backstopped loans such as PPP, is if the bank expects a default tsunami to hit coupled with a full-blown depression that wipes out the value of any and all assets pledged to collateralize the loans.”

Shortly after, the bank also said it would raise its mortgage standards, stating that customers applying for a new mortgage will need a credit score of at least 700, and will be required to make a down payment equal to 20% of the home’s value, a dramatic tightening since the typical minimum requirement for a conventional mortgage is a 620 FICO score and as little as 5% down. Reuters echoed our gloomy take, stating that “the change highlights how banks are quickly shifting gears to respond to the darkening U.S. economic outlook and stress in the housing market, after measures to contain the virus put 16 million people out of work and plunged the country into recession.”

Finally, just days later, JPM also exited yet another loan product, when it announced that it has stopped accepting new home equity line of credit, or HELOC, applications. The bank confirmed that this change was made due to the uncertainty in the economy, and didn’t give an end date to the pause.

In short, JPM appeared to be quietly exiting the origination of all interest income-generating revenue streams over fears of the coming recession, which prompted us to ask “just how bad will the US depression get over the next few months if JPMorgan has just put up a “closed indefinitely” sign on its window.”

On Monday, we got confirmation that it was not just JPMorgan but all US commercial banks that are making the issuance of almost all new credit (with one notable exception) virtually impossible, when the Fed’s July senior loan officer survey showed that banks tightened lending standards across the board for C&I (commercial and industrial loans), CRE (commercial real estate), consumer (credit card and auto loans) and residential real estate (RRE) loans. The loan standards for most products – such as C&I loans, residential mortgages and credit cards – were hiked so much they nearly matched the standards during the financial crisis when it was virtually impossible to get any new loans.

This was the second quarter in a row in which loan officers reported sharply tighter financial conditions.

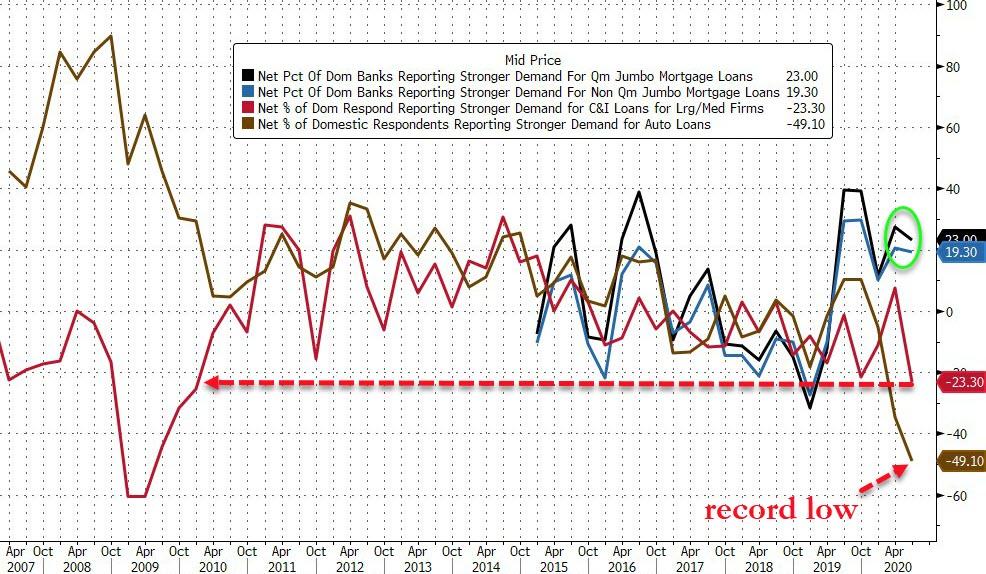

Just as concerning, demand for many loan products also slumped, and in the case of auto loans to record lows, with the exception of jumbo (both conforming and non-confirming) loans, which were roughly flat with demand boosted by record low interest rates.

See: 177 Different Ways to Generate Extra Income

Here are the details:

According to the July Fed’s Senior Loan Officer Opinion Survey (SLOOS), lending standards for commercial and industrial (C&I) loans tightened in the second quarter with a near record 71% of banks on net tightened lending standards for large and medium-market firms (vs. only 42% on net in the previous quarter), while 70% of banks on net tightened lending standards for small firms (vs. 40% on net in the previous quarter). 59% of banks on net increased spreads of loan rates over the cost of funds for large firms, while 54% on net increased spreads for small firms. In short, anything that is not explicitly guaranteed by the government such as PPP loans, banks won’t go near with a ten foot pole for one simple reason: they have zero visibility if and when they will get repaid.

For banks that tightened credit standards or terms for C&I loans or credit lines:

- 22% cited a deterioration in the bank’s capital position as playing a role,

- 97% cited a less favorable or more uncertain economic outlook,

- 85% cited a reduced tolerance for risk,

- 31% cited decreased liquidity in the secondary market for loans,

- 7% cited a deterioration in the bank’s own liquidity position,

- 26% cited increased concerns about the effects of legislative changes, supervisory actions, or changes in accounting standards.

More ominously for a consumer-driven economy, demand for C&I loans from large- and medium-sized firms weakened after strengthening in Q1. 23% of banks on net reported weaker demand for C&I loans for large and medium-market firms, compared to 8% on net reporting stronger demand in the previous survey.

The biggest hit was for commercial real estate (CRE) loans, where standard tightened significantly in Q2. 81% (+29pp) of banks on net reported tightening credit standards for construction and land development loans, 78% (+26pp) on net reported tightening standards for loans secured by non-farm nonresidential properties, and 64% (+15pp) on net reported tightening lending standards for loans secured by multifamily residential properties. Demand for CRE loans fell significantly across all three categories.

While demand for mortgages rose modestly, banks made it more difficult to get a mortgage by significantly tightening lending standards for mortgage loans. Lending standards for GSE-eligible (+53pp to +55%), non-jumbo, non-GSE eligible (+48pp to 59%), Qualified Mortgage jumbo (+50pp to 69%), non-Qualified Mortgage jumbo (+55pp to 70%), non-Qualified Mortgage non-jumbo (+49pp to +64%), and subprime (+29pp to t43%) mortgages all tightened. In other words, all those pleading the case that housing is exploding due to surging loan demand, are forgetting that there is also supply they need to consider, and contrary to conventional wisdom, banks have rarely been less willing to hand out mortgage loans.

Finally, banks’ willingness to make consumer installment loans declined significantly in Q2 (-41% on net vs. -20% on net previously). At the same time, credit standards for approving credit card applications tightened (+72% on net vs. +39% previously), while a modest share of banks also tightened standards for auto loans (+55% vs. +16% previously). Demand for credit card loans declined (-65% on net vs. -23% previously), as did demand for auto loans (-49% vs. -35% previously).

Source: Zerohedge

Subscribe to Activist Post for truth, peace, and freedom news. Send resources to the front lines of peace and freedom HERE! Follow us on SoMee, HIVE, Parler, Flote, Minds, and Twitter.

Provide, Protect and Profit from what’s coming! Get a free issue of Counter Markets today.

Be the first to comment on "It’s Now Virtually Impossible To Get A Bank Loan As Lending Standards Soar"