U.S. Treasury Secretary Steve Mnuchin piled on to comments made recently by President Donald Trump by calling cryptocurrencies a “national security issue.” Bitcoin and crypto proponents more broadly have long wondered if (and how) the government of the United States would recognize the slow but steady encroachment of decentralized assets, and it appears to have begun. Facebook’s announcement of the Libra project on June 18, 2019, will likely prove the point on countless future historical timelines at which the U.S. government began a slow, ultimately ineffective assault upon the cryptocurrency realm.

Everything that Mnuchin attributed to Bitcoin — for one thing, that it has been used in concert with such “illicit activity [as] cyber crime, tax evasion, extortion … illicit drugs, and human trafficking” — can be said, and to degrees an order of magnitude or more larger, about the U.S. dollar. It’s an argument suitable for children.

All of this is extremely bullish for Bitcoin and the entire cryptocurrency complex. A bipartisan political salvo against crypto assets will undoubtedly accelerate the pace of innovation as well as increasing the value proposition, and ultimately the market price, of assets that ensure privacy. Higher prices will draw more crypto developers into the market and direct more resources at capturing market share, which means — as in any market — that consumers are the ultimate beneficiaries.

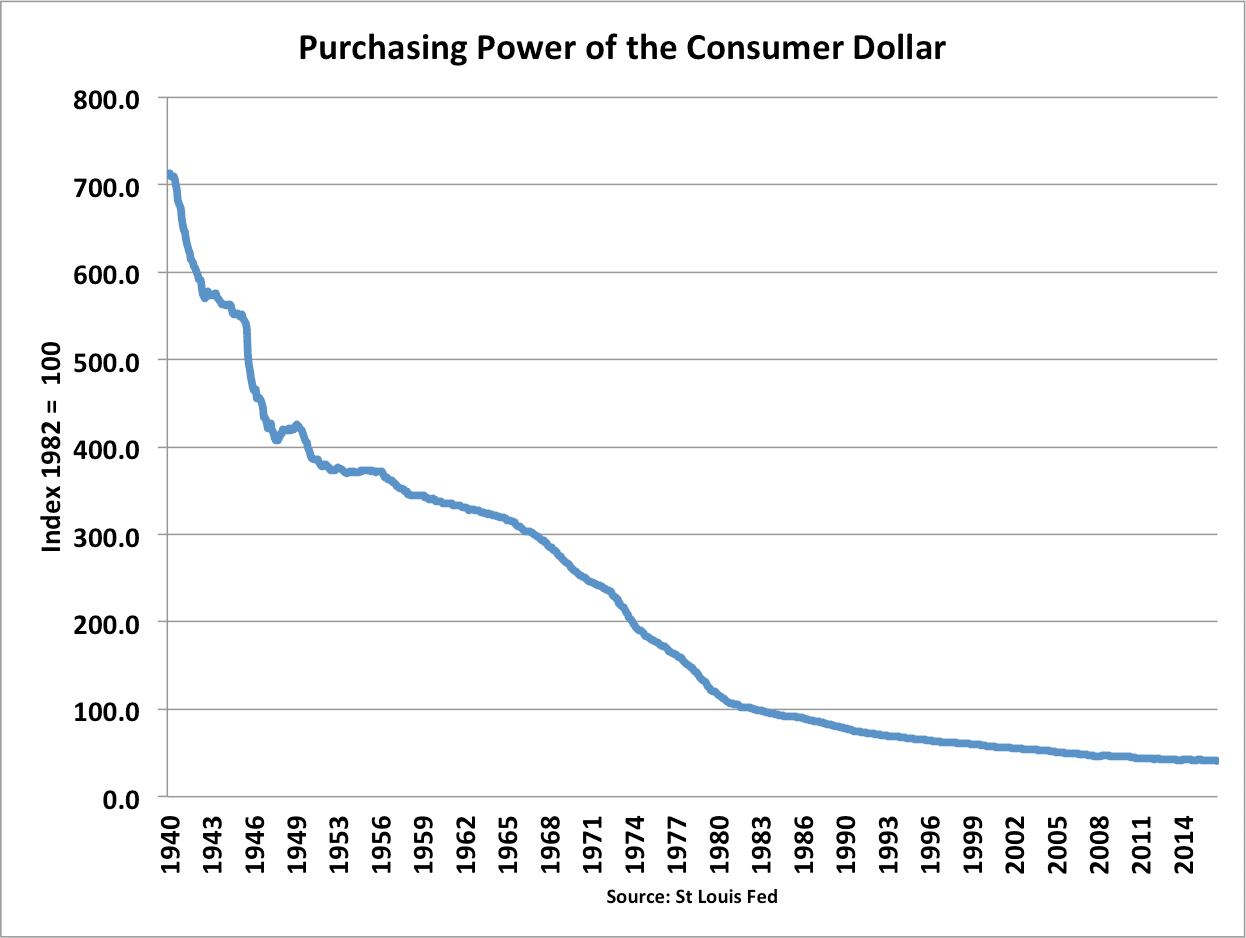

Mnuchin isn’t wrong, though. There is a tremendous risk to American national security where currencies are considered: the dollar. Those who habitually cite its reserve-currency status as a reason not to worry are making an argument that stands on increasingly precarious foundations: since 2010, the U.N. and other groups have cited the dollar’s downward slide in value, urging the adoption of an alternate system of reserves. Earlier this year, the Russian government shifted $100 billion in reserves out of the dollar, into the Chinese yuan. Oil futures denominated in the yuan have been trading for just over one year now, and are steadily gaining liquidity.

The theoretical framework by which the issuer of the reserve currency is at its most secure holds that it is or should be a creditor nation with a current account surplus, but the U.S. is a debtor nation with a current account deficit. More importantly, many have pointed out that the volume of trade is a necessary foundation of reserve status, yet the current administration has both a vocal and policy affinity for interfering with international commerce; the president has famously referred to himself as a “Tariff Man.”

In August 2011 — when the U.S. had a quaint $14 trillion in debt — a crisis over the debt ceiling caused Standard & Poor’s to reduce the credit rating on debt issued by the Treasury. The reduction of the credit rating was tiny, but the knock-on effects were legion. The Dow Jones Industrial Average fell over 2,000 points in the days surrounding the negotiations; within two weeks, a number of Persian Gulf states renewed discussions about diversifying away from the U.S. dollar.

When the pound sterling lost its reserve-currency status to the U.S. dollar, the process took decades: it was an “accumulation of blows” rather than a coup de grace. This is the only realistic way in which such a shift could happen; otherwise, the costs of transacting would suddenly change radically. When the dollar became competitive with the pound, the switch was relatively painless. As the economies of both the Eurozone and China grow, the prospect that either the euro or the yuan — or, more likely, that the similarly disruptive formation of baskets of currencies that include the dollar, albeit in far smaller amounts than are currently held — will take over the dollar’s role becomes increasingly realistic.

Add to this a 20-year war in Afghanistan with no end in sight, a U.S. military presence in over 150 countries worldwide, a mounting willingness to rattle sabers in regions far from domestic shores, and the increasing evidence that the Federal Reserve is not only not independent but highly susceptible to short-term political influence, and the decline of faith in the U.S. dollar becomes understandable. More so when one considers how many thousands of lives, and trillions of dollars, wouldn’t have been squandered under a commodity-backed or cryptocurrency-based monetary system: because it couldn’t have been.

Mnuchin would be well advised to leave market forces to work in their inexorable march toward increasingly sound, more functional iterations of cryptocurrencies and other decentralized digital assets, and to shift his attention toward the countless political factors that are eradicating the last vestiges of faith and credit in the dollar. If the current path is maintained (and quite possibly even if it isn’t), the future belongs to truly “dependable and reliable” monetary media: cryptocurrencies and precious metals.

{kind=link}

{kind=link}

{kind=link}

Sign up here to be notified of new articles from Peter C. Earle and AIER.

Peter C. Earle is an economist and writer who joined AIER in 2018 and prior to that spent over 20 years as a trader and analyst in global financial markets on Wall Street. His research focuses on financial markets, monetary issues, and economic history. He has been quoted in the Wall Street Journal, Reuters, NPR, and in numerous other publications. Pete holds an MA in Applied Economics from American University, an MBA (Finance), and a BS in Engineering from the United States Military Academy at West Point. Follow him on Twitter.

This article was sourced from AIER.org

Image credit: Pixabay

Subscribe to Activist Post for truth, peace, and freedom news. Follow us on Minds, Twitter, Steemit, and SoMee.

Provide, Protect and Profit from what’s coming! Get a free issue of Counter Markets today.

Be the first to comment on "The Dollar, Not Crypto, Is a National Security Issue"