1 – The US stock market is slightly overbought (which is not a positive in terms of head room for more of a rally).

2 – It’s massively built up on debt that is now more expensive to maintain and/or obtain.

3 – The Fed is still rapidly tightening money supply and says it will continue to do so for several more months.

4 – Interest rate increases and money tightening that already happened through this past December will continue to worsen economic conditions until summer because any changes by the Fed have about a half year lag time for the general economy.

5 – That also means all the tightening that continues between now and September, will continue to pile more and more weight on top of the economy until next February, which is why the Trump admin. is screaming the Fed went too far.

6 – 2019 Q1 US corporate earnings are coming in almost as poorly as economists said they would, and they don’t look set to start rising much in the next quarter … if at all.

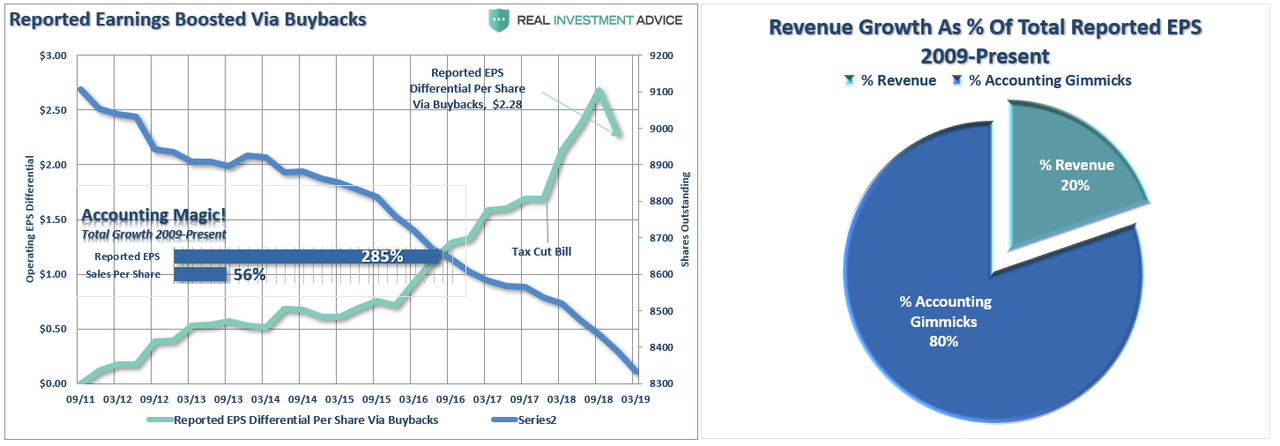

7 – Measures used to help earnings beat much lower expectations (and not by much) were mostly cost-saving measures, not revenue boosters, or they were mere accounting choices. Earnings are after-tax numbers, so they benefited hugely in 2018 from the Trump Tax Cuts in a way that had nothing at all to do with companies doing better business. They are also reported as a “per share” number, and the main thing that changed was the number of outstanding shares in the denominator as a result of stock buybacks. So, really, earnings were pathetic!

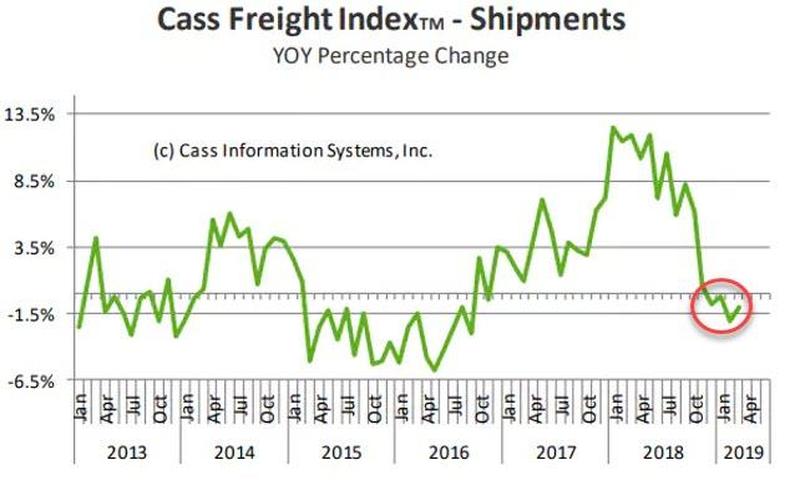

8 – Transportation is declining as product shipments decline. West-coast port imports plunged 19% from the previous quarter (3% YoY). Trucking lost ground four months in a row.

9 – Manufacturing is slowing in the US and Europe. PMI plummeted in the US to a 31-month low, taking us back to the Obama era. Businesses reported significant slowing in output, new orders, and hiring. China had a March growth spurt but only because of a massive stimulus pump. China injected 200-billion yuan of liquidity in one shot into its economy, and interest rates still jumped up.

10 – Business inventories are growing while sales are declining, meaning production has to slow more than it already has because back pressure is building.

11 – US interest rates inverted COMPLETELY on the gauge the FED uses to estimate recession risk (3-month rates over ten-year rates), which has been the Fed’s most reliable indicator of a coming recession.

12 – Major cash from repatriation is starting to dwindle, while stock buybacks using cash and cheap credit were the only fuel pushing the US market upward most of the last ten years. (Take buybacks out of the equations, and the market would have been flat at best.)

13 – US government debt is soaring as far as the eye can see at the highest rate of increase we’ve ever seen, meaning the government cannot do any more than it is already doing.

14 – Existing stimulus effects from the Trump Tax Cuts have been waning each of the last two quarters. US GDP for the first quarter of 2019 is estimated to be substantially lower still, meaning the tax cuts, after more than a year, are grossly failing to perform as promised while they are not paying for themselves either. The IMF and World Bank have projected a decline in global GDP over the full year.

15 – The Fed is highly reluctant to turn back to more quantitative easing and rate reduction and, thereby, REALLY prove it couldn’t do what it claimed it could and would. Therefore, it will be late in helping and more limited in the help it can provide, forcing it to more extreme and reckless experiments in novelty monetary policy when it does jump back in.

16 – US unemployment is bottoming out, which it always does immediately before a recession, with an increase in the last couple of months, although there was also blip of decrease in reported filings at the end of March.

17 – Housing has been in steady decline across the USA for more than half a year now, and prices have finally begun to fall to coincide with the declining sales. Housing starts and permits in March took another tumble, and February’s bad figures, thought to be a one-off due to bad weather, were just revised from an 8.9% plunge to a devastating 12% crumpling heap. Australia’s housing market looks like the US market did just as the US market took down the world. The UK and Canada are having problems, too.

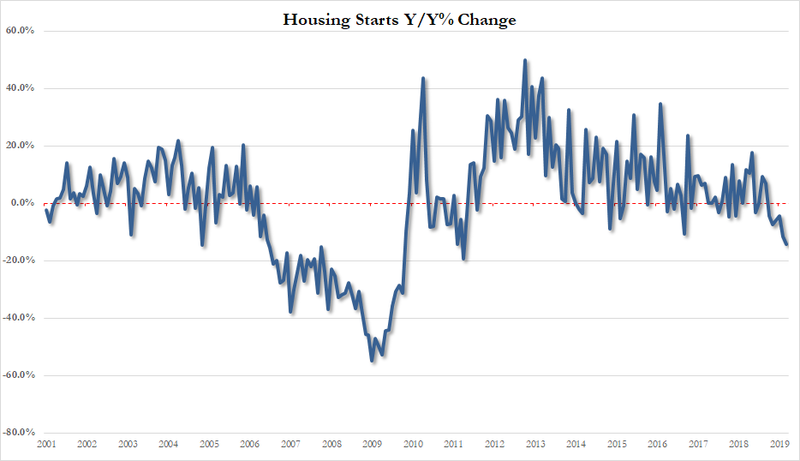

18 – Retail sales growth, including autos, have been in continual decline for months, though there was a bounce in March. More retail stores (nearly 6,000) have already closed in the first quarter of this year than closed in all of last year or the year before, and those years were pretty bad. More auto factories are closing, too.

19 – March’s improvements on the metrics above may just be a rebound after the government shutdown, while December-February’s lows would have been abnormally lower due to the shutdown, too, which makes something between January/February stats and March stats the place we’re actually stuck in, which is still not good.

20 – Any trade deal with China appears likely at this point to come out limper than a boiled wanton as negotiations drag on after promise and promise of summits that fail to deliver or fail to even happen.

21 – John Bolthead and Mike Pompous have likely scuttled any hope of a North Korean nuclear deal … if there ever was any hope. As you recall, the nuclear Cold War was weighing on the stock market many months ago when rhetoric and nuclear activity last heated up.

22 – The stock market is back at its highest peak level, which may make investors skittish at this point, given the major crashes that happened the last two times it got into this stratosphere. This is a perilously high ceiling of resistance to break through. (Of course, if it does break through and holds, it could soar.)

23 – Just as before the dot-com crash, the values of many high-tech companies / online companies are based on soft metrics, such as “number of daily users” or “volume of user interactions,” rather than hard profits; and there is a lot of fantasy in some of those narratives.

24 – Inflationary pressures are backing off, but deflationary pressure is more indicative of a recession than inflation as deflation happens when demand recedes and growth stalls. Lower inflation also presses the Fed back to interest reduction and more quantitative easing, which it doesn’t want to do, lest it underscore the fact that we are stuck forever in money-printing mode just to hold against a receding tide, and where the Fed doesn’t have much room to move.

No wonder the Fed, as laid out in my last Premium Post, is paving the path for significant fundamental changes in how it does business in a world of economic conditions that it says have changed forever.

Liked it? Take a second to support David Haggith on Patreon!

This article was sourced from The Great Recession Blog.

Provide, protect and profit from what is coming! Get a free issue of Counter Markets today.

Be the first to comment on "List of 24 Points Pressing Hard Toward Recession"