This is not about Liberating Oppressed Peoples, it is about Establishing Global Maritime Supremacy & a Chokehold on World Trade

I had written an article several months back discussing the real agenda behind Trump’s enthusiastic backing of the sale CK Hutchison’s Panama ports to BlackRock early 2025.

What many were not aware of, was that BlackRock stood to gain not only two Panama ports from this deal with the Hong Kong based company CK Hutchison, but 41 other strategic ports.[1] In other words, the deal was for BlackRock to purchase 43 out of its total 53 ports (the only ports not included in this deal were located in China).

BlackRock is the world’s largest asset manager with over $11.6 trillion under its belt, the acquisition promised $1.7 billion in annual revenue, marking a bold expansion into infrastructure from its more traditional ventures in stock and bond investments.

BlackRock had been officially brought in by the Biden Administration to manage the Global Infrastructure Partners (GIP) as a direct counter to China’s Belt and Road Initiative (BRI), originally titled by Biden as “Build Back Better World.”

Who owns GIP? BlackRock does. Thus, BlackRock, which manages the assets of billionaires, has been directly working with the G7 countries in open opposition to China’s BRI. In other words, infrastructure around the world is getting purchased by BlackRock such that it will be privately owned and managed by a billionaire class.

In fact, Eric Van Nostrand, a BlackRock managing director who was head of research for sustainable investments and multi-asset strategies joined the Biden Treasury Department and worked as a senior adviser on economic issues tied to Russia and Ukraine.

Not so coincidentally, Zelensky later announced in 2023 that the world’s largest investment company would be in charge of creating a fund for rebuilding Ukraine…which was BlackRock.

Included in this roster for a “Build Back Better World” was Chairman and CEO of Microsoft Satya Nadella.

The Biden White House FACT SHEET states:

“Microsoft and BlackRock each highlighted billions in investment in support of PGII priorities, including Microsoft investing nearly $5 billion in digital infrastructure, cybersecurity, skilling, and other capacity building in Kenya, Indonesia, and Malaysia, plus additional infrastructure investments and other initiatives in Thailand and the Philippines.”

Thus, this is effectively a BlackRock and Microsoft led endeavour in the execution of the G7’s Partnership for Global Infrastructure and Investment (PGII), which is part of GIP, as a counter to China’s BRI…

Nothing concerning about that arrangement, right?

What that means is BlackRock manages trillions of dollars of wealth that is primarily owned by billionaires around the world. Its job is to find out ways to invest the money of the rich so that they can become wealthier. BlackRock has traditionally invested in stocks and bonds (with its counterpart Blackstone investing in infrastructure). However, with BlackRock’s recent venture into investment in infrastructure globally, what this amounts to, is the acquiring and privatization of key strategic infrastructure globally to service the billionaire class.

These key infrastructures will be privatized under BlackRock and will charge a fee for their use.

On matters of geopolitics, counterintelligence, revisionist history and cultural warfare.

What most people do not realise is that Trump’s tariffs were meant to work towards this very same agenda of global acquisition. If all had gone according to “plan,” Trump would not have needed to use “the big stick,” in Teddy Roosevelt’s words – but countries dared to embarrass the U.S. by dragging their feet, others outright opposed the “deals” that had been so “generously” put on the table. U.S. Secretary Treasury Scott Bessent had warned the world repeatedly, that essentially, resistance would be futile, and if any nation dared to retaliate, there would be heavy consequences.

One very serious and dangerous form of retaliation that continues to loom over the Trump Administration’s hegemony are nations’ dumping their holdings of U.S. Treasury bonds.[2]

Last April 2025, Japan dared to do this. Prime Minister of Japan Shigeru Ishiba had strongly opposed America’s insulting “deal” that was put before them. Accept American GMO rice when Japan produces their own higher grade non-GMO rice, buy America’s lower standard in quality and safety cars at the cost of Japan’s own car industry and adjust their currency to encourage purchases of American goods to the detriment of Japan’s economy which is already literally on life-support after decades of acquiescing to “deals” with the U.S. Remember the Plaza Accord anyone?

In addition, Japan was being urged to shun strategic trade with China, such as in semiconductors, which would also seriously hurt their own industry and heavily invest into becoming an Asian NATO as America’s strong arm against China.

US Billionaires Unite to “Make America Great Again”

Is Japan Willing to Cut Its Own Throat in Sacrifice to the U.S. Pivot to Asia?

Ishiba even went so far as to write a letter to Xi assuring China that Japan wanted to maintain healthy trade relations despite pressure from the United States.

Where is Shigeru Ishiba now? Gone. Japan has a new Prime Minister now, Sanae Takaichi who seems more than willing to bend the knee. On that note, Shinzo Abe is the only Japanese Prime Minister to remain so for more than three years since 2006. In other words, over the past 19 years, Japan has gone through 11 Prime Ministers, including Abe who acted as Prime Minister for a total of about nine years. For the rest of those ten years, Japan went through ten Prime Ministers!!! That should tell you something about Japan’s state of affairs. It should also maybe tell you something about why Abe was assassinated…

Why Shinzo Abe Was Assassinated: Towards a ‘United States of Europe’ and a League of Nations

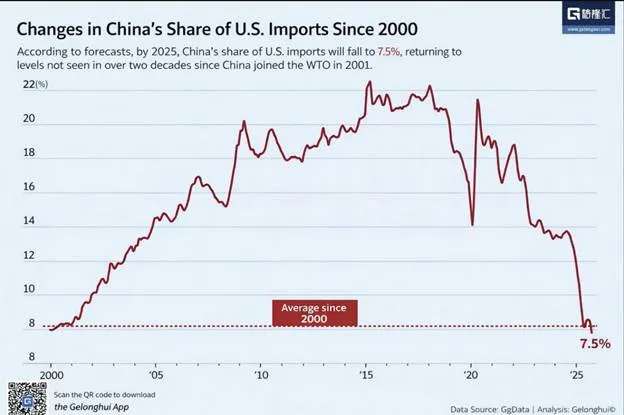

There were many countries that did not agree upon a “deal” with the U.S. including India (until recently), Taiwan, Mexico, Canada, Brazil, and very notably China, the most important country of all and the reason why the tariffs were launched in the first place. If China were to fall, the entire global resistance to U.S. economic hegemony would not have a hope in the world. Thus, if the U.S. wanted to secure its status as world hegemon, they would need to contain China.

In fact, because the tariffs have been unable to contain China after one year of economic warfare, you could say it is official, the U.S. tariffs have failed in achieving their goal, which was to bring the world’s largest exporter to its knees and subservient to the United States consumer market and dollar hegemony.

Don’t believe this was the true agenda? Just ask your friend Peter Navarro, White House advisor on economics who told Vietnam zero tariffs for the U.S. won’t cut it. What was he asking for? Forfeiting all trade relations with China.

Countries around the world were being told, or rather threatened, to make a choice between the United States or China in their trade relations. If they dared to favour China over any trade relations, the U.S. would penalise them through tariffs. It was an attempt to have the entire world turn its back on China. Not only this but demand their industries in service to the United States’ crusade to save the world from an “unbalance” in Chinese exports.

However, the horrifying truth is that the American economy has been hit harder, way harder, than China has after one year of this approach towards world domination.

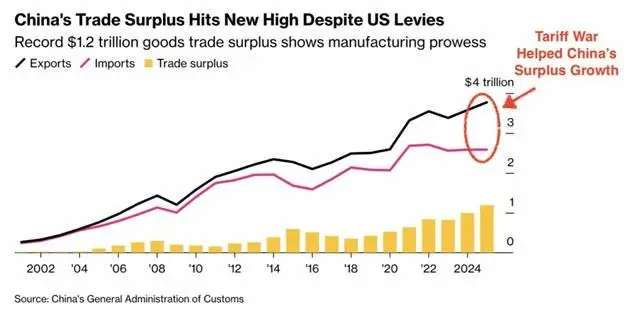

China actually had a record year in export surplus at $1.2 trillion. What this means is that China actually exported more in 2025 than in any other year, with overall exports increasing by 6.6% in December. This is despite their exports to the U.S. decreasing by about 25%. In other words, in less than one year, China was able to replace the U.S. consumer market, a feat that Scott Bessent thought outright impossible.

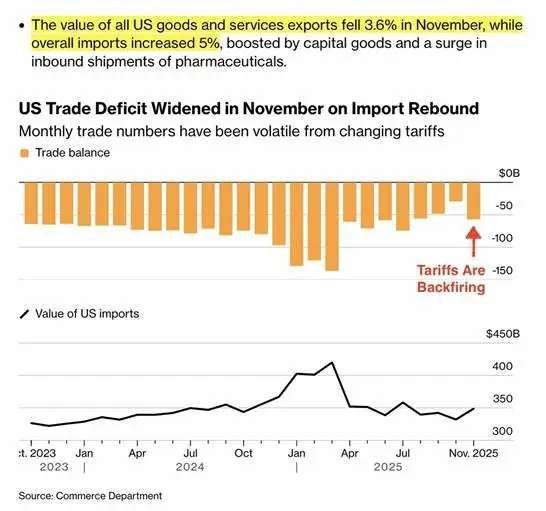

Not only this, but the U.S. had in fact inflicted damage onto its very own economy from its own weaponised tariffs!

At the end of 2025 the results were in, U.S. exports had in fact DECREASED the very opposite of what the tariffs were supposed to achieve, while imports continued to rise. Thus, America was still dependent on the world for its consumption…but the world was looking like it was not dependent on America.

A huge factor in the U.S. actually dropping in its total exports in 2025 was, of course, China. This was not the fault of China, the U.S. tariffs had been put in place against the country hoping it would cause China to cave and beg for mercy. Instead, China simply walked away.

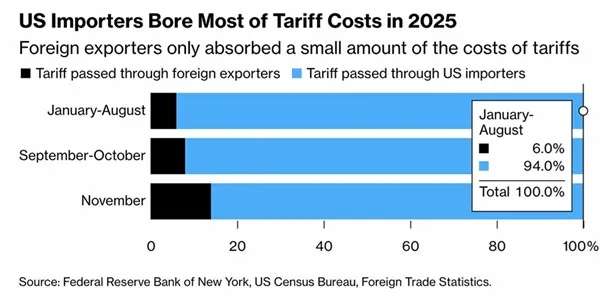

In addition the jury is also out on who indeed “ate the tariffs” in 2025, as many feared, it was the United States’ businesses, consumers and manufacturing base.

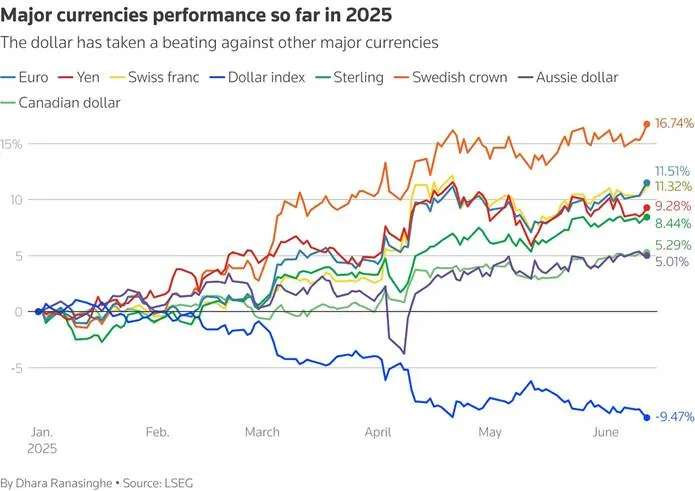

The knife was plunged ever deeper with the status of the USD.

The USD dropped to record lows as all other world currencies appreciated.

Yes, you want a lower USD if you want to encourage exports but if you also need a significant amount of your material imported for manufacturing reasons (which is the case for the U.S.) this can be a double-edged sword. You also want a strong enough USD such that it remains as the reserve currency.

But China, along with its increase in exports to the world is also asking countries to pay in RMB (Renminbi), that is, the Chinese currency the Yuan. Increasingly China is moving itself towards the position of becoming the world’s reserve currency. As more countries trade in RMB the world moves closer to dedollarization and threats of sanctions by the United States are starting to sound more and more like mouse squeaks rather than loud growls.

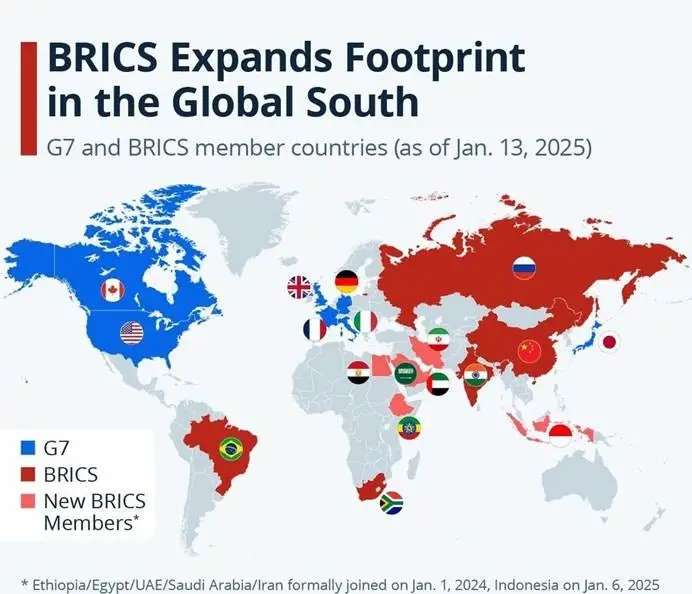

In fact, the tariff war, though China was the main target, was to target the BRICS nations as a whole, which have been working together to counter America’s weaponization of the reserve currency in the form of endless sanctions.

BRICS’s original members since 2010 are Brazil, Russia, India, China and South Africa hence the acronym. Since then, Egypt, Ethiopia, Iran, and the UAE have joined as official members in 2024. Argentina dropped out and Saudi Arabia is still sitting on the fence. Indonesia joined in 2025 bringing the total members to 10 countries. Observer states which are not yet officially part of the BRICS but expect to join in the future are Belarus, Cuba, Kazakhstan, Malaysia, Thailand, Uganda, Uzbekistan, and Nigeria, among others.

The BRICS is thus an alliance of countries that have formed to counter the G7’s over-dominance on world policy and economic development and advocate for the self-determination of the “Global South.”

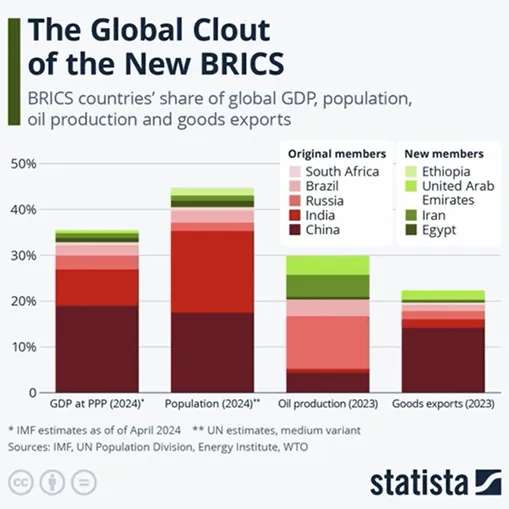

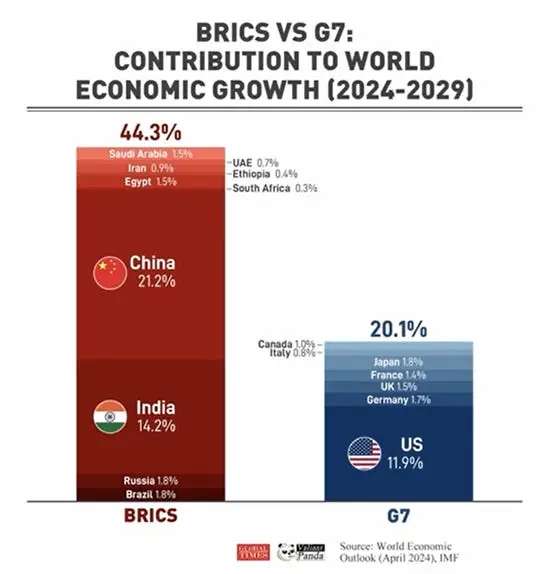

As the American and European economies are faltering due to their own policy decisions, the BRICS nations are growing exponentially. It does not take a rocket scientist to see which way the wind is blowing here.

This throws a big wrench into the G7 plan and all their machinations. The idea of course was to control the Global South with the established financial system. You use your dollar sanctions and weaponized Swift system to ensure compliance. But if the majority of GDP (manufacturing, energy, demand) belong to BRICS – then G7 loses any power to dictate over the Global South.

And the Southeast Asian countries are especially growing fast with big consumer markets.

Thus, the United States entered 2026 with quite the chill up its back. Its worse fear had come true, it was becoming irrelevant. After all of its blowing and blustering in 2025, the Trump Administration did not have much to show for it in terms of Roman tributes, its economy was faltering and its dollar was slipping.

Here is where Venezuela, Iran and Greenland come in.Subscribe

Case Study Number #1 in U.S.’s bid for Global Domination: Venezuela

Though we can say that the actions of Trump in just the first few months of 2026 – the kidnapping of the President of Venezuela Nicolás Maduro and the bombing of Iran along with Israel and the murder of the Ayatollah, during negotiations, are most definitely connected to America’s dismal economic performance last year, these objectives were always in the cards. It is just the speed and ferocity in meeting these objectives that has changed.

Some have compared the United States to a cornered animal at this point. The only way to counteract its massive show of economic weakness in its abysmal performance last year and maintain its King of the Jungle status is to show a great deal of physical force in the year 2026. ‘Might makes Right’ didn’t you know? The mask has been lifted earlier than planned.

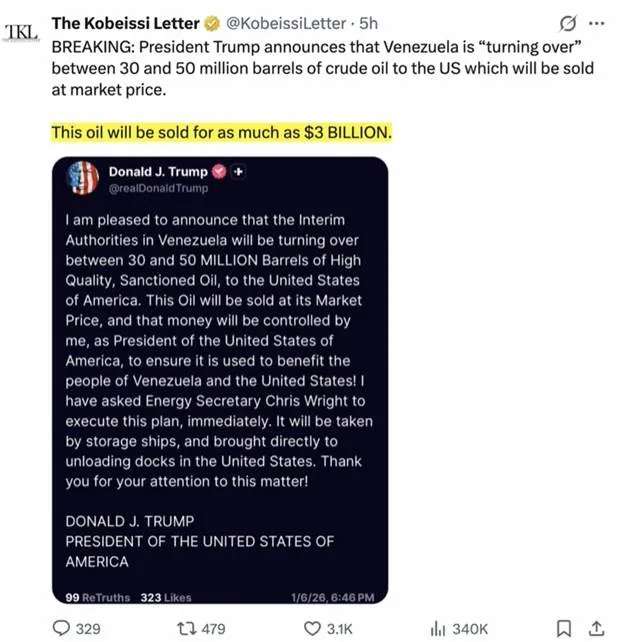

In case you didn’t get the memo, Venezuela was never about cracking down on the drug cartels, it was about the oil. Has anyone heard of what the U.S. is doing to address the drugs coming out of Venezuela since the kidnapping of Maduro? No, of course not. Why would the U.S. crack down on the drug cartels when they have put so much time and money into putting them there in the first place?

The CIA’s complicity in the Mexican Drug Cartels (including military training at Fort Bragg)

Instead we heard about Trump giving a tour to CEOs of Big Oil – which didn’t go over very well by the way.

So much for the drug cartels….

But Trump got a stark wake up call with the acquisition of Venezuela, besides the fact that there is internal resistance to his dictating how the country should be run along with its oil (surprise surprise) – there was another caveat to this fantastically swift take-over of the largest oil reserve in the world – its infrastructure was dilapidated after decades of sanctions and economic warfare that had been waged by the very United States itself. Ironic isn’t it?

It turns out to rebuild Venezuela’s crude oil infrastructure it will cost over $10 billion PER YEAR over the next decade. Where is this money going to come from? The current sales of Venezuelan crude will not be able to pay for this level of investment. The U.S. would be going into the negative to achieve this.

Not only this but guerilla attacks are a very real threat and companies like ExxonMobil have already lost their oil infrastructure in Venezuela to such attacks.

There is also no guarantee that the political atmosphere in Venezuela and its people will tolerate such a blatant American occupation of their land. It is for this reason that the Big Oil CEOs, like ExxonMobil, have walked away from this mess that the Trump team appears to have put together as a real ad hoc operation inspired by the scriptwriters for “The A-Team.”

There is also the issue of the quality of Venezuelan crude, it is a low-quality oil that is not easy to process and refine. Many countries are not specialized in refining Venezuelan crude.

America is specialized in processing crude oil, but they are also producing their own supply of crude. The objective was to try to corner the energy market, but other than the United States, China is one of the few who specializes in refining Venezuelan crude oil. There is a reason why Venezuelan crude is sold at a discount, it isn’t just because of the sanctions. Venezuelan crude is the most challenging and expensive to refine.

Of course, a big reason, or you could even say the reason for the U.S. clamouring to claim Venezuelan oil was the hope of gaining leverage on China.

In fact, Venezuela owes China money for infrastructure investments that had been agreed to be paid by oil at a discount (by the way the U.S. had been receiving its oil from Canada at a 20% discount and for nothing in return before the tariff war). However, Trump is trying to play a game with China, that they are simply not interested in playing.

Not to mention that the UK once again “freezes” a country’s assets, this time conveniently timed with Maduro’s kidnapping – recall Russia’s asset seizure.

UK Foreign Secretary Yvette Cooper said they did this for “democracy”, right…..

This is of course sending a very strong message to other countries. Your assets are also not safe if you decide to make a move that is not approved by Anglo-America.

When the G7 sanctions froze and eventually seized Russia’s Central Bank Reserves it started a daily chain of events that accelerated to move towards a multi-polar world. It also escalated the global dumping of U.S. dollar assets….

But the United States has not given up just yet on smashing that square peg into a circle.

The power-crazed giddiness was palpable after the Maduro kidnapping. First threats on sanctions for Chinese companies and tankers with Venezuelan links, in Trump’s attempt to address the shadow fleets that have grown in numbers thanks to the U.S.’s asinine sanctions (more on this shortly) and then turning around and demanding China buy Venezuelan oil from the U.S. at the price they set.

Such antics the U.S. fantasises will make China “desperate” to make a “deal.” Instead, it looks like they are just running circles around themselves.

One very big reason why the U.S. wants China to buy the oil through them, be it American or its newly acquired Venezuelan oil, is because they will be able to dictate the terms of the sale, namely that it be done through USD, to maintain U.S.’s petrodollar status. Afterall, China was buying 90% of Venezuelan crude.

Its looks like the lesson is not going to be learned anytime soon…

Why did U.S. exports in crude oil decline last year? Because China used to be the second biggest importer of U.S. crude. Woops!

And China has many alternatives to Venezuelan oil as well.

The United States has once again put itself in a rather embarrassing predicament. They do not have the buyers for their Venezuelan crude along with its dilapidated structure that will take $100 billion or more to build, not even U.S. Big Oil is interested, and now storage tanks of oil are rotting away with nowhere to go…

Case Study #2 Europe, the Blowing up of Nordstream & Russia’s Shadow Fleet

Europe is now the second largest importer of U.S. crude and I am sure they are not thrilled about it.

China has cut away their imports on U.S. oil by 46%. U.S. oil from Chinese companies fell from 150 million barrels to under 82 million. And this knocks China down from the second biggest importer to number six. This makes Europe the second biggest destination for U.S. crude now. And the number one purchaser of U.S. LNG.

Reuters writes: “From 2018 through 2021, U.S. LNG exports to Europe averaged around 15 million tons a year, according to Kpler, but jumped to around 55 million tons annually in 2022 and 2023 as Europe’s power firms scramble to replace lost Russian gas by whatever means necessary.” And at a much higher cost.

By 2028 the U.S. wants to almost double their LNG export capacity. And those are the blue bars in the below chart. And an additional 10 billion cubic feet per day is expected to come online in the next four years. Unlike Russia whose cost of production is much lower, the U.S. needs to keep demand for their energy high. So if BRICS consolidates and gets all their energy or at least most of it from the Middle East and Moscow, U.S. Energy producers are going to be in trouble.

In order to fulfill this demand, the U.S. needs Europe as a captive customer more than ever.

And I do mean captive…

Gas flows from Nord Stream have stopped completely. And just below it on the map, the flow to Yamal via Poland has also ended. So zero gas is entering the EU from these two pipelines. And what we have left is gas going through the Turkstream and the Ukraine transit. If those are closed, that’s it for cheap pipeline energy going into Europe.

I am sure the U.S. is very happy with their decision to blow up the Nord Stream pipeline so that Europe is now dependent for the foreseeable future on expensive American LNG, a European energy market that would not have given the Americans the time of day otherwise.

How America Took Out The Nord Stream Pipeline

And it looks like things are going to get a whole lot more desperate…

The Hungary-Slovakia-Ukraine oil dispute is an ongoing major diplomatic and energy crisis between Slovakia, Hungary and Russia vs Ukraine. It began last year, triggered by the expiration of the Russia-Ukraine gas transit contract.

As of January 27, 2026 the Ukrainian transit has been compromised, particularly the Druzhba pipeline, the only pipeline of Russian oil into Europe. Hungary and Slovakia are the only remaining refineries in the EU using Russian oil through the Druzhba pipeline. They have been trying to resecure the oil flow after it was stopped on Jan. 27 after what Ukraine dubiously claims was a “Russian drone attack.” Sure. However, all major news outlets appear to recognise that this was indeed an attack made by Ukraine.

Ukraine has already made it clear they do not want to continue receiving Russian energy since they think it benefits Russia – apparently unaware that it is greatly benefiting them as well. Hungary, a Russian ally, is clearly not buying Ukraine’s story and is threatening to cut off power and gas exports to Ukraine unless Kyiv resumes Russian oil shipments.

This halt cuts roughly 5% of the EU’s total gas supply, heavily concentrated in Central and Southern Europe, who were put in a position this past January where they needed to find alternative energy routes ASAP or face a cold and dark winter.

Croatia began attempting to source their oil through their Adria pipeline as Slovakia and Hungary’s only remaining lifeline. However, since then Slovakia and Hungary have reported Croatia to the EU that Croatia is using their situation as a monopoly to charge fees three times higher than the European average. This has triggered a legal battle in the European Commission.

However, the EU itself is not favorable to receiving cheap energy from Russia and has been in the process of pressuring EU countries to phase out their use of Russian LNG through the Turkstream pipeline. In the midst of a very serious energy crisis with soaring energy costs, countries are understandably not in any hurry to do this.

In the first eight months of 2024, 100 terawatt hours of energy was shipped through the Ukraine transit. And that is equivalent to 5% of EU total gas imports and that is half of total Russian pipeline gas going into the EU. In 2024, France, Spain and Belgium accounted for 85% of Europe’s Russian LNG imports.

And in the first half of 2025 the EU imported €4.48 billion in Russian LNG, an increase of €3.47 billion over the same period the year prior. Thus, European countries were in fact increasing not decreasing their purchase of Russian energy last year, despite all of the heavy-handed political pressure and scary threats not to do so.

However, no need to fret. The European Commission has successfully passed its plans to phase out all Russian gas and oil imports by 2028 a few months ago (October 2025). Under the proposal, new contracts would be prohibited from January 1, 2026. Existing short-term contracts would end by June 17, 2026, and long-term contracts would be banned from January 1, 2028. What could go wrong?

Hungary and Slovakia are the only EU countries that still import large amounts of Russian oil. Convenient timing for a drone attack isn’t it?

However, if this cheap gas supply goes away, Europe will have to replace this with more expensive options which is going to be U.S. LNG, especially now that Qatar’s LNG is out of commission for the foreseeable future in supplying Europe’s needs thanks to the U.S. launching a war with Iran. Convenient timing once again?

How feasible is this energy plan for Europe amidst calls to rebuild European industry, and what appears to be a growing investment in military buildup?

But even this accelerated timeline does not seem to be fast enough according to the desires of Anglo-America in there now fully exposed war for global energy dominance.

With the bombing of Iran which would lead to the very predictable closing of the Hormuz Strait and Iran’s predictable retaliatory response in targeting Qatar’s LNG and Saudi Arabia’s oil (Or was it an Israeli attack blamed on Iran?), is the U.S. hoping that everyone will scramble over each other to buy American oil and LNG at astronomical prices, willing to sell their own grandmother to make a “deal” and kiss the ring?

Not only this, but it appears radical scarcity in energy is the goal in this new global order.

It should be noted that Russian intelligence suspects a plan to blow the Turkstream and Bluestream pipeline, as reported by the Kyiv Independent news agency.

“Our operational information is being reported. It concerns a possible explosion of our gas systems at the Black Sea’s bottom,” Putin said during a meeting of Russia’s Federal Security Service board.

TurkStream and Blue Stream are major undersea pipelines transporting Russian natural gas directly to Turkey and Europe, bypassing transit routes through Ukraine. The infrastructure plays a key role in maintaining Russia’s energy exports.

And whether Brussels wants to admit it or not, the European continent is still very much powered by Russian energy. If Europe entirely shuts down their access to Russian energy – China and other Asian countries are going to win big. Gazprom will be forced to send more of their supply eastwards which will push prices down for Beijing. Basic supply and demand. That ironically puts further pressure on western industries. Now Chinese goods will become even more affordable.

On that note, India’s tentative recent deal with the U.S. to buy Venezuelan crude and shun Russian oil is also disastrously shortsighted.

If India is indeed foolish enough to give this up, they are heading towards much higher energy costs with longer travel periods and if it is coming from Venezuela, a great deal of unknown in what lies in the future. Meanwhile this could not come at a more perfect time for China who would rather Russian oil which is higher quality, cheaper to refine and a lot less hassle to import. And if India drops Russian oil, this means China can buy more at a cheaper price. Simple supply and demand.

China dumping U.S. oil isn’t good, and Russian energy leaving the EU is even worse, for the west that is. But the U.S. is apparently doing everything it can to speed up this process in the deluded fantasy that they will somehow be holding all of the cards in the end.

Since the Ukraine War, the U.S. Treasury has imposed sweeping sanctions on Russia’s oil production and exports and the list is exhaustive, punishing Gazprom and other suppliers, targeting 180 shipping vessels, oil traders, service providers and insurance companies.

The U.S. and the West have sanctioned a record number of Russian tankers, or tankers covering Russian oil, at least 270 tankers. And if they transport Russian crude their companies will be locked out of the Western system. And any companies that might deal with them might be punished as well. Their assets might also get confiscated away.

However, despite all of these threats, Russian oil has still been reaching its destinations. This revelation is from the EU themselves who have been tracking Russian oil and volumes.

The Russian shadow fleet, a clandestine network of ship vessels to evade sanctions, is shipping Russian oil to three main destinations China, India and to a lesser degree, Turkey. However, countries like Singapore, Bulgaria, UAE, Brazil, South Korea and the Netherlands are also receiving shipments as well.

As we can see from the Figure 6 graph above, Russian shipments in oil via seaborne routes have been increasing not decreasing. Since 2022 it is on an uptrend from under a million barrels a day to over 3 million. That’s a 300% increase which is a clear sign that the sanctions aren’t working. And you can blow up as many pipelines as you wish, Russian crude is still going to reach its destinations via the seas.

Notice in the Figure 6 graph that the routes via the Arctic ocean are the fastest growing. Could this be why the United States is obsessed with claiming Greenland along with establishing a NATO base. That the massive danger to the world that Russia and China pose in navigating the Arctic ocean is shipments and trade in affordable energy?!?

However, the U.S. is really adamant on fitting this square peg into a circle, and thus more sanctions have been put in place against Russian energy last year. The absurdity of this approach is that it isn’t really hurting Russian revenue, but it is spiking energy cost for economies around the world.

The above Figure 7 graph is showing stats from 2024, EU was receiving at the time 30% of Russian crude. The sanctions have been hurting western economies the most, just like the U.S. tariffs hurt the American economy the most and European economies second. Trying to block and dictate world trade with financial penalties is backfiring badly.

And where is this 30% now going to be heading do you think – China and the rapidly growing region of East Asia. It turns out Asia does not need the business of the United States or Europe. Tisk tisk.

And as energy costs soar for the West from their own decisions, manufacturing costs are also going to soar, where is the money going to come from? Products manufactured will in turn be more expensive and more slowly produced than in Asia, how is the West to compete with less and more expensive energy?!?

Here is where we come back to BlackRock’s attempt to acquire 43 of the strategic ports from CK Hutchison.

One very obvious way Anglo-America could clamp down on Russia’s Shadow Fleet is to control all major ports in the world. By controlling these ports, they can dictate the terms, the fees that will need to be paid if the ship is granted permission to dock. In fact, why stop at sanctioned ships, when you can heavily tax whoever you choose.

In fact, the Trump tariffs are aimed to be used in this manner against, you guessed it, China.

Reports have been made that a fee will be charged to the operator at a rate of up to $1.5M or based on the percentage of Chinese-built vessels in that operator’s fleet. For operators with 50% or greater of their fleet comprised of Chinese-built vessels, the operator will be charged up to $1M per vessel entering a U.S. port.

To be clear here, this is not aimed at even Chinese trade at this point. It is aimed at any company that has purchased a Chinese ship to transport their goods. The company could be American, European or Australian it doesn’t matter. If the company is using Chinese transport ships they face heavy penalty fees.

This is because China is by far the lead producer in cargo ships, while the U.S. is essentially a non-factor. For every 359 large container ships China makes, the U.S. produces one each year. The U.S. wants to change that. How are you going to become a maritime superpower if everyone is buying Chinese container ships?

This is once again extremely destructive. These companies have already invested heavily in already made purchases and are now going to be penalised for any attempt on expanding their trade since they will have no choice but to buy Chinese container ships because NO ONE ELSE IS PRODUCING THEM in the quantity needed to facilitate world trade!!! The U.S. is planning on heavily taxing these companies for the crime of using a Chinese container ship, when the U.S. doesn’t even make enough to facilitate its own trade. This is going to seriously backfire on trade with the U.S. not the world.

CMA CGM is a French company, Hapag-Lloyd is a German company, HMM is a South Korean company, Maersk is a Danish company, MSC is an exception in this since they are part of the diabolical BlackRock deal (see my paper for more on this), ONE is a Japanese- Singaporean company, Yang Ming is a Taiwanese company, ZIM is an Isreali company.

In order for this not to backfire on the U.S. economy, you would need to control all major ports in the world to put adequate pressure on these shipping companies. The BlackRock deal was just that, though for now, the purchase has been successfully blocked by China. Likely the plan is to forcibly seize these strategic port locations that are not under the mandate of Anglo-America, as they did in Panama.

If the U.S. can successfully acquire these ports, this will also dissuade buyers from future purchases of China’s container ships. Meanwhile, theoretically, the U.S. will gradually fill this vacuum with their own ship manufacturing base, which presently, is practically non-existent. Great plan.

Of course, there does not seem to be a care of what happens to world trade in the meantime. Since when has ‘controlled scarcity’ not been a good thing for a Great Reset? The only way the U.S. is going to catch up with China’s supply chain is through a Molotov cocktail, you didn’t think the U.S. was planning on winning a fair fight when it is so much easier to just blow things up?

It is like the game Monopoly, at least this is the dream of Trumpian America, you buy (or seize) ports around the world hope a Chinese ship lands on them and they have to pay you a hefty tax. However, did it ever dawn on them that new ports would simply be made in such a world?

If this fantasy were to become reality (which is unlikely) a thousand Chinese ships docking at these U.S. controlled ports would mean a billion dollars in revenue for the U.S. economy, I mean, military. Who are we kidding here.

In the second instalment we will discuss Case Study #3 Greenland & Case Study #4 Iran along with some concluding thoughts.

Cynthia Chung is the President of the Rising Tide Foundation and author of the books “The Shaping of a World Religion” & “The Empire on Which the Black Sun Never Set,” consider supporting her work by making a donation and subscribing to her substack page Through A Glass Darkly.

Watch our other RTF and CP films and documentaries here.

On matters of geopolitics, counterintelligence, revisionist history and cultural warfare.

[1] To my knowledge, this deal has largely been blocked by China since (except for the two Panama ports which have been recently seized).

[2] A country, or private investors within a country, can decide to sell off their holding of US treasury bonds for several reasons, one of them being a low-confidence in the US economy’s growth as well as low confidence in the US’ ability to pay back their debt, which would mean a lower return and higher risk of return to the investor. A rising Treasury Yield indicates falling demand for Treasury Bonds which are the bedrock of what prevents the US from defaulting on their massive debt. For more on this see my paper.