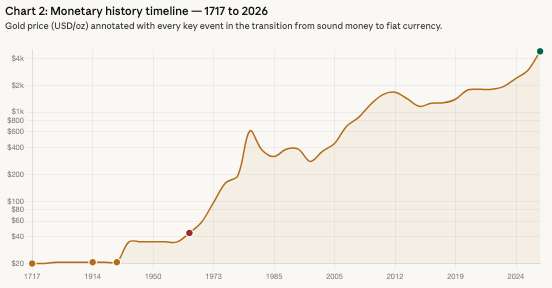

The Man Who Priced Gold for 200 Years

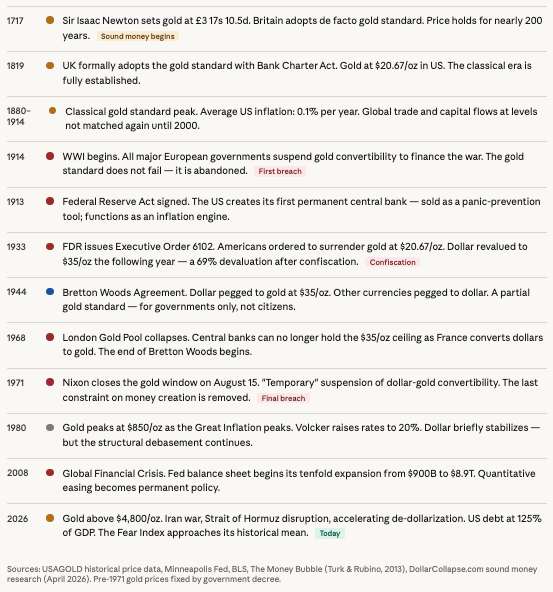

Most people recognize Sir Issac Newton for his work on gravity, but in 1717, he was more than a great scientist. He was Master of the Royal Mint of England, and he had a problem to solve:

What should an ounce of gold be worth in British pounds?

Newton sat down, did the math, and set the price at 3 pounds, 17 shillings, and 10.5 pence per troy ounce. He did not form a committee…

There was no press conference to shape “perception.” And no models were built on assumptions about “inflation expectations.” One man, one number, anchored to physical reality.

That price held, more or less, for nearly two centuries.

In those same two centuries, the world went from candlelight to electricity. From horse carts to steam locomotives. From local village markets to a truly global economy that, by 1913, was as integrated as a share of world GDP as it would be again in the year 2000. From hand-stitched clothing to textile factories running 24 hours a day. The Industrial Revolution, the great burst of human productivity that lifted more people out of poverty than any event in recorded history, unfolded entirely under a monetary system where the pound, the mark, the franc, and the dollar were simply different names for fixed weights of gold.

We know what sound money looks like. We lived under it for two hundred years. We thrived under it. And then we threw it away.

What the Gold Standard Actually Was

Before we can understand what we lost, we have to kill a myth. The gold standard is not remembered accurately. Most people picture it as rigid, primitive, deflationary, the monetary equivalent of a corset. It was none of those things.

The mechanics were elegant. Every major national currency was convertible into a fixed weight of gold. The Bank of England, the anchor of the global system, held 40 percent gold reserves to back the British pound. Anything less was considered reckless. Long-term interest rates were low and stable, because when money cannot be printed, there is no inflation premium baked into the bond market. Investors lend at low rates when they trust that the pounds or dollars they get back will buy roughly what the pounds or dollars they lent away bought when the loan was made.

The money supply grew at approximately 1.8 percent per year, matching world population growth and new wealth creation. No central bank committee voted on this. No chairman gave a press conference about it. Geology enforced it. New gold mining could only add so much metal to the aboveground stock each year, and that natural constraint kept the purchasing power of money stable across generations.

Milton Friedman spent much of his career arguing for what he called the k-percent rule: that monetary stability requires the money supply to grow at the same modest, predictable rate each year. Gold achieves Friedman’s ideal automatically, through physics and chemistry, without any human institution or political process required. No fiat currency has ever come close to matching it.

Consumer prices during the classical gold standard era did not rise year after year. In many periods they fell modestly, as technological improvements made production more efficient. This meant that savings actually gained purchasing power over time. So, thrift made sense. Long-term planning made sense. A worker in 1880 could make a financial commitment that would still make arithmetic sense in 1900, because the unit of account he was using had not been quietly debased while he slept.

What Two Centuries of Sound Money Produced

This is the part of the story that modern economics textbooks do their best to obscure, because it is simply too damaging to the case for central banking and fiat currency.

The Industrial Revolution happened under the gold standard. Railroads crossed continents under the gold standard. The telegraph, steam shipping, the mechanization of agriculture, the rise of a global middle class, all of it happened under a monetary system where the money supply was governed by geology rather than by the discretion of appointed officials.

By 1913, global capital flows were enormous. British investment financed railroads in Argentina, mines in South Africa, and factories in the United States. German industrial firms raised capital across European borders. American entrepreneurs tapped London’s financial markets. All of this cross-border investment required a shared monetary framework, a common language of value, and gold provided exactly that. A gold-backed pound and a gold-backed dollar were not two different monetary promises. They were two different denominations of the same thing.

The result was the greatest sustained expansion of real living standards in human history. Not the greatest expansion of financial assets. Not the greatest expansion of credit. The greatest expansion of actual human welfare: calories consumed, children surviving infancy, life expectancy, literacy, physical mobility, access to goods that would have seemed miraculous to prior generations.

It was not a perfect system. Recessions happened. Bank panics happened. The business cycle was not abolished. But when downturns came, they cleared. Bad debts were liquidated. Inefficient enterprises failed. The economy adjusted and moved on. There were no multi-decade zombie recoveries propped up by central bank balance sheet expansion. There was no “secular stagnation.” There was no “new normal” of 2 percent growth that gradually became accepted as the permanent ceiling of human economic ambition.

The gold standard did not promise a world without hardship. It promised a world where money told the truth. That, it turned out, was enough to produce something close to economic paradise by any historical standard.

The Beginning of the End

The gold standard did not fail. It was abandoned…

Here’s the difference:

When the guns of August 1914 opened fire on the plains of northern France, every major European government suspended gold convertibility within weeks because war is expensive, and gold is finite. You cannot finance industrialized mass slaughter on an honest money supply. If the British Treasury had been required to back every new pound it issued with gold, the war would have ended by Christmas 1914, not by the exhaustion of a generation.

So the governments printed. And the world that had been built on two centuries of sound money began its long, slow, and at times violent unraveling.

The waypoints are worth marking because each one was presented, at the time, as a temporary, necessary, pragmatic response to an emergency. Each one turned out to be permanent.

In 1913, the United States created the Federal Reserve, the first major institutional breach of the sound money principle in America. In 1933, Franklin Roosevelt issued Executive Order 6102, requiring American citizens to surrender their gold to the government at $20.67 per ounce. The following year, having collected the gold, the government revalued it to $35 per ounce, a 69 percent devaluation executed after the confiscation was complete. Citizens who obeyed the law were made immediately poorer. The Bretton Woods agreement of 1944 created a partial gold standard for governments while denying gold convertibility to ordinary citizens. And then, on August 15, 1971, President Nixon went on television to announce that the United States would “temporarily” suspend the convertibility of the dollar into gold.

That temporary suspension has now lasted 55 years.

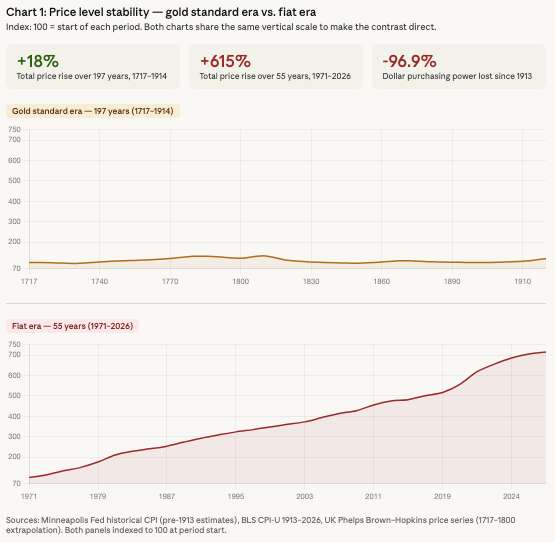

Both charts use a price index where 100 represents the starting point of each era, meaning every number you see is a measure of how far prices have moved relative to that baseline. The gold standard panel, covering 197 years from 1717 to 1914, barely moves, peaking at 118 and troughing as low as 95, a range so narrow it appears almost flat. The fiat currency panel, covering just 55 years from 1971 to 2026, climbs from 100 to 715, meaning the cost of the same basket of goods has risen more than seven times over in little more than half a century, a rate of debasement that would have been considered a civilizational catastrophe under any prior monetary standard.

What Abandoning Sound Money Has Cost

The numbers, at this point, speak more clearly than any argument.

The dollar has lost more than 95 percent of its purchasing power since the Federal Reserve was created in 1913. M2 money supply has expanded by approximately 80 percent per decade since 1960.

80 percent per decade.

Every generation of American workers has watched the purchasing power of their savings cut roughly in half during their working lives, not by any market event or democratic vote, but by the quiet, continuous operation of a monetary system that answered to no geological constraint and faced no meaningful political accountability.

The United States national debt today stands at 125 percent of GDP. Private credit default rates have reached 9.2 percent, matching levels last seen during the 2008 financial crisis. The Federal Reserve, having expanded its balance sheet nearly tenfold since 2008, is now trapped: it cannot raise interest rates enough to genuinely fight inflation without crashing the bond market, the stock market, and the government’s own financing costs simultaneously. The monetary authorities call this a “difficult environment.” It is, more precisely, the predictable arithmetic consequence of replacing sound money with the promises of politicians and appointed officials.

Now, markets work fine when prices tell the truth, but this is the failure of a monetary system that was designed, from the moment the gold constraint was removed, to transfer wealth from savers and workers to governments, banks, and debtors, and to do so invisibly, continuously, and with no democratic mandate.

We Know the Answer

Here is the thing about the optimistic reading of this story:

It is also the accurate reading.

The solution to what ails the global monetary system is not theoretical. And it hasn’t been dreamed up by economists in a seminar room. It ran the world for two centuries and produced the greatest expansion of human prosperity ever recorded. It was enforced not by any government promise or central bank policy, but by the laws of nature. Gold cannot be printed. Silver cannot be conjured by committee. The supply of honest money grows at the rate geology permits, which happens, as Milton Friedman observed, to be almost exactly the rate that a well-functioning economy requires.

The Bank of England understood this. For most of the classical gold standard era, it held 40 percent gold reserves to back the British pound. Its governors considered anything less to be reckless. That standard, applied to today’s US M3 money supply, would require a gold price of roughly $29,000 per ounce. Even a 20 percent backing, far below the Bank of England’s historical standard, would require gold at around $16,000.

Gold above $4,800 today, the highest nominal price in history, is no a bubble…

Gold’s price is the market’s attempt to price in eight decades of accumulated monetary debasement, with the current Iran crisis and the accelerating de-dollarization of global energy trade acting as catalysts for a process that was always going to arrive eventually.

Sound money works. History spent two centuries answering that question. Soon, we may have the wisdom forced on us, and the political will, to choose it again before the current system forces the choice upon us in far more painful circumstances.

Newton set the price of gold in 1717 and it held for nearly 200 years. We abandoned it in stages between 1913 and 1971. We have spent the 55 years since paying the tab.

At some point, the tab gets paid in full.