President Donald Trump wants a lower US dollar. He complains about the over-valuation of the American currency. Yet, is he right to accuse other countries of a “currency manipulation”? Is the position of the US dollar in the international monetary arena not a manipulation in its own right? How much has the United States benefited from the global role of the dollar, and is this “exorbitant privilege” coming to end? In order to find an answer to these questions, we must take a look at the monetary side of the rise of the American Empire.

Trump is right. The American dollar is overvalued. According to the latest version of the Economist’s “ Big Mac Index,” for example, only three currencies rank higher than the US dollar. Yet the main reason for this is not currency manipulation but the fact that the US dollar serves as the main international reserve currency.

This is both a boon and a curse. It is a boon because the country that emits the leading international reserve currency can have trade deficits without worrying about a growing foreign debt. Because the American foreign debt is in the country’s own currency, the government can always honor its foreign obligations as it can produce any amount of money that it wants in its own currency.

Yet the international reserve status comes also with the curse that the persistent trade deficits weaken the country’s industrial base. Instead of paying for the import of foreign goods with the export of domestic production, the United States can simply export money.

American Supremacy

The performance of the US economy in the 20th century owes much to the predominant role of the US dollar in the international monetary system. A large part of attaining this role was the result of the political and military supremacy that the United States had gained after World War I. Still today, the position of the US dollar in the world of finance represents a major underpinning of the prosperity at home and provides the basis for the expansion of the US military presence around the globe.

After each of the two world wars in the 20th century, the United States emerged as the largest creditor country, while the war had ruined the economies of the war-time enemies along with that of the major allies. After the end of the Cold War, this pattern would experience a repetition. The United States, so it seems, has been, since then, the only remaining superpower.

In the 1990s, the dollar experienced a new flourishing, and the US economy went through magical rejuvenation. However, this time the economic and political fundamentals gave much less support to the assumed role of the dollar in the world. In contrast to the time after World War II, the basis for the dollar’s global expansion in the 1990s was not economic strength, but debt creation. The public debt ratio, which had been falling since the end of the war began to turn-around in 1982 and has been rising ever since (Figure 1).

Figure 1: US Gross Federal Debt Ratio (Debt in percent of gross domestic product), 1940–2018. Source: US Bureau of Public Debt, tradingeconomics.com

With this debt creation came a new phase of global expansion of the dollar. The spread of the dollar provided the basis for the economic performance and the military position of the United States. Yet this time, the new structure that has emerged is outwardly powerful but inherently fragile. It is not economic strength that provides the foundation of the role of the US dollar in the international monetary system, but it is the US dollar’s financial role that provides the basis for the United States to maintain and extend its global activities.

While after 1919 and after 1945, the United States emerged not only as the largest international creditor, but also as the major industrial power, the US has become an international debtor since the 1980s and is confronted with a weakening industrial base. Also, in contrast to the earlier world wars and the other conflicts, the economies of Russia, Western Europe, and Southeast Asia did not lay in ruins when the Cold War ended. As to their productive capacity and financial resources, these regions now are on an even footing with the United States.

For a while it appeared as if the international monetary system that emerged in the 1990s could be interpreted as a new version of the older Bretton Woods System whose structure foresaw a central role for the US dollar in the post–World War II era. While the parallels fit insofar as the current system provides similar benefits to the participants, the present structure is even more flawed than the older scheme, which broke down due to its inner contradictions.

Bretton Woods

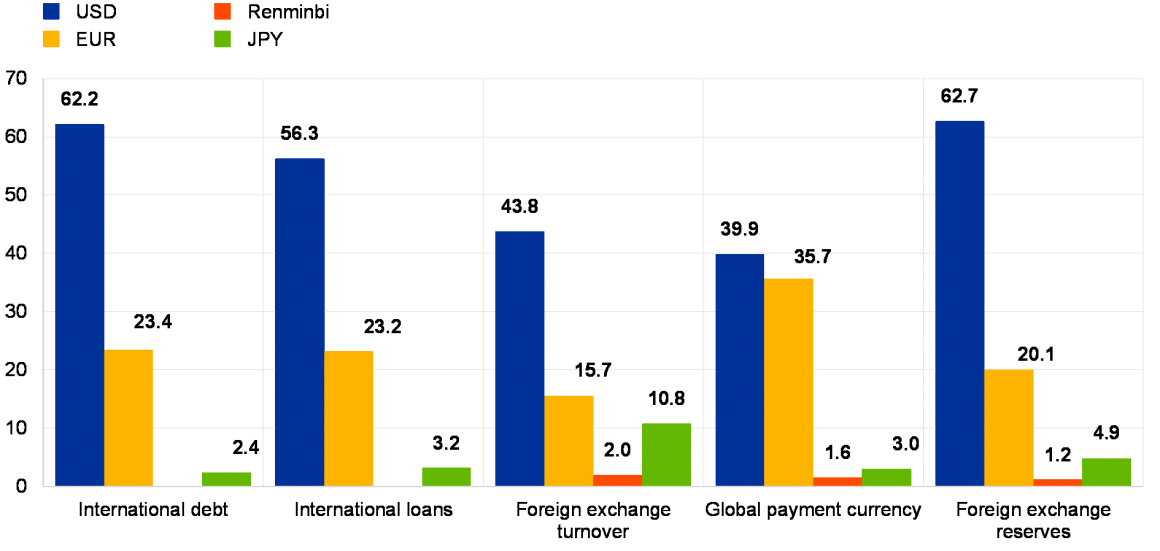

Like the earlier Bretton Woods System (BW1), the current system (BW2) is characterized by the pegging of foreign currencies to the US dollar or using the dollar as the currency of reference. This time, it is mainly Southeast Asian countries, particularly China, that practice this policy in an informal way. Through this arrangement, these economies in Southeast Asia receive a similar advantage as was once enjoyed by the Western European countries when their undervalued currencies gave them a competitive advantage that helped to rebuild their industrial base after the Second World War. Once this reconstruction stage was completed, the BW1 system fell apart, and the Europeans began to build their own currency system. The decoupling of the European currencies from the dollar progressed step by step and finally led to the introduction of the euro in 1999. As of now, the euro is equal to the US dollar in the size of its internal use, yet as a global currency, and particularly as an international reserve currency, the US dollar still dominates majestically (Figure 2).

Figure 2: Shares of the major currencies in the international monetary system. Source: European Central Bank

Mainly the central banks in Southeast Asia, foremost China, have accumulated US dollars as their international reserves in the recent past. However, there is little doubt that their willingness to finance US deficits and to hold on to a weakening currency will not last forever. As happened in Europe before, once the prime goal of these countries is fulfilled — industrial development based on exports with the help of undervalued currencies — Southeast Asia will move out of the dollar linkage.

The Bretton Woods System as it was established by the end of World War II bestowed an “exorbitant privilege” to the United States when the dollar became the point of reference for the international currency system following the Bretton Woods Accord. With the other member countries fixing their currencies to the US dollar, and the US dollar officially fixed to gold at $35 per troy fine ounce, it seemed as if an ideal construction was found in order to avoid international monetary disruptions and to provide the framework for global economic expansion.

The gold anchor was aimed at preventing an excessive production of US dollars by the US government. When foreign countries had a trade surplus, they were formally allowed, according to the Bretton Woods Accord, to exchange the excess dollars for gold from the American Treasury. With a stable parity between dollar and gold, this would have restricted dollar creation. France took the agreement literally and demanded gold from the United States instead of accumulating dollars as international reserves. Yet other surplus countries such as Japan and West Germany refrained from that option. With their exchange rates kept competitive, Japan and West Germany embarked upon an export-led growth strategy that sped up their economic recovery and made them industrial powers again.

For the United States, the BW1 system provided a special privilege and it did not take long for the United States to abuse it. Pursuing the goal of expanding the welfare state along with ever-more-active foreign military involvements, the United States expanded the money supply drastically. The discrepancy began to widen between the stock of gold in the vaults of the Federal Reserve and the dollars in circulation in the world. It became obvious that the US government no longer had the means to fulfill the original agreement of making foreign currencies exchangeable into gold. By the late 1960s, the dollar shortage of the 1950s had turned into a dollar glut. World price inflation began its rise.

Originally in the BW1 treaty, it was stipulated that the modification of currency parities should be an exception rather than a rule. But in the course of the 1960s, the international monetary system entered into a phase of high instability when fixing and re-fixing of foreign currencies to the dollar became a huge concern. The perverse monetary system that emerged created a bonanza for currency speculators. The candidates for exchange rate revaluation — such as Germany or Japan — were easy to identify. By taking out a dollar loan and changing the money at a fixed rate into German marks or Japanese yen and then depositing the amount, leverage could be applied, and profits were guaranteed when the revaluation of the foreign currencies occurred — as it was not hard to foresee. The risk was minimal and largely confined to bearing the cost of the interest rate differential between the rate of the dollar loan and that of the deposit rate in the German or Japanese money markets.

Long Live the Dollar

In the late 1960s, the international monetary system had transmogrified into a source of global liquidity creation that originated from the United States but forced also other nations to import this inflation. Inflation-fighting central banks, such as the German Bundesbank, could not effectively apply restrictive instruments. Given that the interest rate differential was the prime risk factor for currency speculators, a restrictive monetary policy with higher interest rates in the revaluation candidate country would attract even more hot money and would have made the speculation even less risky. Central banks abroad, particularly the German Bundesbank and the Bank of Japan, massively accumulated US dollars as international reserves when they held their exchange rates fixed to the dollar at the undervalued parity. Yet by buying up the excess offer of US dollars with their own currency, these countries expanded their own monetary base and laid the foundation for inflation at home.

In 1971, with the so-called “Smithsonian agreement,” a final attempt was made to save the old system when the United States devalued its currency against gold and a series of other currencies. However soon thereafter, it became obvious that there was no chance of revival for the old regime. In 1973, with the adoption of the new rule that each country could choose its own currency arrangement, the Bretton Woods System was officially declared as dead.

Since then, the US dollar has entered into a long decline, interrupted by two episodes. Under the Reagan presidency, the Cold War entered into its final period, and the dollar became the currency of refuge for some time. The US victory in this battle appeared as a replay of the endings of World War I and World War II with the United States emerging for a third time on top of the world. In the 1990s, the triad of global dominance seemed well in place for the United States: unrivalled military might, a booming and innovative economy, and the status of undisputed issuer of the global currency. The US dollar experienced another period of strength. Since 2002, however, the long-term trend toward a weaker dollar is back in place, interrupted by lower peaks of the waves of strength (see Figure 3).

Figure 3: US Dollar Index, 1965–2019. Source: tradingeconomics.com

The Dollar and US Foreign Policy

In the 1990s, the monetary policy of the United States became an instrument of a grand geostrategic enterprise. The neoconservative movement took this constellation as it emerged in the 1990s for granted and implemented a policy that was based on a philosophy that assumed with almost religious confidence that it was the duty and right of the United States to be the hegemon in the 21st century. In contrast to the time after the two world wars, however, the rest of the world outside of the United States did not lay in ruins. While after the two world wars, it was the US industrial base that laid the foundation for the role of the US dollar, now it was not the superiority of the US industrial base that provided the basis for the global role of the United States but its insatiable appetite for private and public consumption. The current underpinning of the geostrategic supremacy play of the United States is the US dollar by itself in its role as the major international reserve and trade currency. It is a system without a proper foundation similar to traditions that live on for some prolonged period of time even when the reasons for their existence have vanished.

Changing of the Guard

The easy monetary policy of the United States has accelerated the de-industrialization at home and has fostered industrialization abroad (predominantly in China and in the rest of Southeast Asia); it has produced a situation that stands in sharp contrast to the end of World War I and World War II. Under the new BW2 system, the United States is no longer the largest creditor with the largest industrial base, but instead has become the largest international debtor. Imperial politics requires expansive monetary policy, and the consequence of it shows up in persistently high trade deficits and a deteriorating external investment position (Figure 4).

Figure 4: United States net international investment position, 1976–2019 (in million US-dollars). Source: tradingeconomics.com

Being the issuer of a global currency provides huge benefits that come with a curse. Increased private and public consumption possibilities come from the privilege of getting goods from abroad without the necessity of producing an equivalent amount of tradable export goods. While other countries have to export in order to pay for their imports, the sovereign who emits a global currency is exempt from adhering to the most fundamental law of economic exchange. This sets domestic resources free for the expansion of the state, particularly military power. The more such an imperial power extends its military presence, the more its currency becomes a global currency, and thereby new expansionary steps can be financed. Expansion becomes a necessity.

Over time, however, the divergence widens between the weakening industrial base at home and the extended global role. With goods coming from abroad for which there is no immediate need to pay with sweat and effort, the domestic culture changes from an ethics of production to hedonism. Creeping corruption cronyism undermines the political system. With resources set free because of imports, the production of goods at home shifts to fancy activities. The cycle of “panem et circenses” has been the fate of all empires.

The current global position of the United States is similar to that of Spain in the period of its decline. Already economically hollow, Spain tried desperately to hang on to its outposts and “possessions” around the globe while the domestic economy transmogrified into a public-service and militarized economy. In the end, the United States gave the coup de grace to the Spanish Empire by taking away Cuba, Puerto Rico, and the Philippines. A new phase of US geographic expansion and dominance began and in 1898 and the stage was set for the United States to become the imperial power of the 20th century.

History, and in particular economic history, always shows both: common features and differences, and indeed, the American Empire is different from some of the former empires. Yet what the United States has in common with the former imperial states is that at some point the military extension becomes too complex to be handled efficiently and thus becomes too costly.

The discrepancy between the relative position of the US economy in the world on the one hand and the relative position of the United States as to its military presence and the role of the US dollar on the other hand is moving toward a cracking point. This leads to the conclusion that in a world where the economic strength of the United States is diminishing relative to other countries and regions, there will be less and less of a place for the US dollar privilege.

Different from the factors that justified the expectation of a coming demise of the dollar in 2007, the American currency has experienced a new spring due to the financial crisis of 2008. With little else in place for shelter, the US dollar served as a safe haven. It remains to be seen if this will also be the case when the next financial disaster happens.

Dr. Antony P. Mueller is a German professor of economics who currently teaches in Brazil. Write an e-mail. See his Amazon author page.

Note: The views expressed on Mises.org are not necessarily those of the Mises Institute.

This article was sourced from Mises.org

Subscribe to Activist Post for truth, peace, and freedom news. Follow us on Minds, Twitter, Steemit, and SoMee. Become an Activist Post Patron for as little as $1 per month.

Provide, Protect and Profit from what’s coming! Get a free issue of Counter Markets today.

Leave a comment

You must be logged in to post a comment.

Be the first to comment on "Why the Dollar Rules the World — And Why Its Reign Could End"