Michael Snyder

Michael Snyder

Activist Post

Most people have no idea that the U.S. financial system is on the brink of utter disaster. If interest rates continue to rise rapidly, the U.S. economy is going to be facing an economic crisis far greater than the one that erupted back in 2008. At this point, the economic paradigm that the Federal Reserve has constructed only works if interest rates remain super low. If they rise, everything falls apart. Much higher interest rates would mean crippling interest payments on the national debt, much higher borrowing costs for state and local governments, trillions of dollars of losses for bond investors, another devastating real estate crash and the possibility of a multi-trillion dollar derivatives meltdown.

Everything depends on interest rates staying low. Unfortunately for the Fed, it only has a certain amount of control over long-term interest rates, and that control appears to be slipping. The yield on 10-year U.S. Treasuries has soared in recent weeks. So have mortgage rates. Fortunately, rates have leveled off for the moment, but if they resume their upward march we could be dealing with a nightmare scenario very, very quickly.

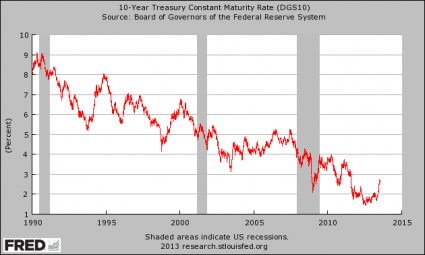

In particular, the yield on 10 year U.S. Treasuries is a very important number to watch. So much else in our financial system depends on that number as CNN recently explained…

Indeed, since May, just before Bernanke announced a probable end to QE3, the yield on 10-year Treasuries has jumped around almost one percentage point, to 2.6%, wiping out more than two years of interest payments. The markets clearly fear that far higher long-term rates are lurking in the absence of exceptional policies to rein them in.

That’s a crucial issue, because those rates are highly influential in determining the future performance of stocks, bonds, and real estate. Investors grant equities higher multiples when long-term rates are lower; both longer-maturity Treasuries and corporate bonds jump when rates decline; and developers pocket more cash flow from their projects when they borrow cheaply, raising the values of office and apartment buildings. When rates reverse course, so do all of those prices the Fed has been endeavoring to swell as a tonic for the economy.

Even though the yield on 10-year U.S. Treasuries has risen substantially, it is still very low. It has a lot more room to go up. In fact, as the chart posted below demonstrates, the yield on 10-year U.S. Treasuries was above 6 percent back in the year 2000…

And the yield on 10-year U.S. Treasuries should rise substantially. It simply is not rational to lend the U.S. government money at less than 3 percent when the real rate of inflation is about 8 percent, the Federal Reserve is rapidly debasing the currency by wildly printing money and the federal government has been piling up debt as if there is no tomorrow…

Anyone that lends the U.S. government money at current rates is being very foolish. You will end up getting back money that has much less purchasing power than you originally invested.

Why would anyone do that?

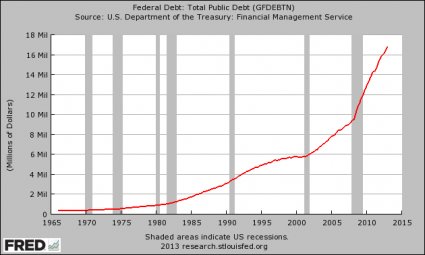

But if interest rates rise, the U.S. government could be looking at some very hairy interest payments very rapidly. For example, if the average rate of interest on U.S. government debt just gets back to 6 percent (and it has been far higher than that in the past), the federal government will be shelling out a trillion dollars a year just in interest on the national debt.

State and local governments all over the nation could also very rapidly be facing a nightmare scenario.

Detroit is already on the verge of formally declaring the largest municipal bankruptcy in the history of the United States, and there are many other state and local governments from coast to coast that are rapidly heading toward financial disaster even though borrowing costs are super low right now.

If interest rates start rising dramatically, it would cause a huge wave of municipal financial disasters, and municipal bond investors would lose massive amounts of money…

“Muni bond investors are in for the shock of their lives,” said financial advisor Ric Edelman. “For the past 30 years there hasn’t been interest rate risk.”

That risk can be extreme. A one-point rise in the interest rate could cut 10 percent of the value of a municipal bond with a longer duration, he said.

Many retail buyers, though, are not ready for the change and “when it starts, it will be too late for them to react,” he said, adding that he was encouraging investors to look at their portfolio allocation and make changes to protect themselves from interest rate risks now.

In fact, bond investors of all types could be facing monstrous losses if interest rates go up dramatically.

It is being projected that if U.S. Treasury yields rise by an average of 3 percentage points, it will cause bond investors to lose a trillion dollars.

And already we have started to see a race for the exits in the bond market. A total of 80 billion dollars was pulled out of bond funds during the month of June alone. If you want a visual of the flow of money out of the bond market, just check out the chart in this article.

We are witnessing things happen in the financial markets that have not happened in a very, very long time.

We are witnessing things happen in the financial markets that have not happened in a very, very long time.

And junk bonds will be hit particularly hard. About a decade ago, the average yield on junk bonds was about twice what it is right now. When the junk bond crash comes, there is going to be mass carnage on Wall Street.

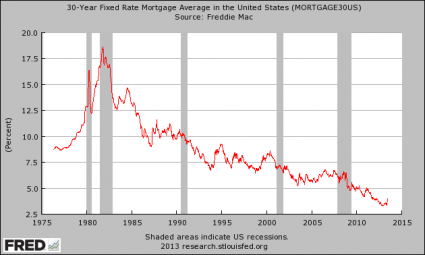

But of much greater importance to most Americans is what is happening to mortgage rates. As mortgage rates rise, it becomes much more difficult to sell a house and much more expensive to buy a house.

According to CNBC, there is an increasing amount of concern that the rise in mortgage rates that we are witnessing could throw the real estate market into absolute turmoil…

The housing recovery is in for a major pause due to higher mortgage rates. It is not in the numbers now, and it won’t be for a few months, but it is coming, according to one noted analyst. The market has seen rising rates before, but never so far so fast; there is no precedent for a 45 percent spike in just six weeks. The spike is causing a sense of urgency now, a rush to buy before rates go higher, but that will be short term. Home sales and home prices will both come down if rates don’t return to their lows, and the expectation is that they will not.

We have seen the number of mortgage applications fall for four weeks in a row, and at this point mortgage applications have declined by 28 percent over the past month.

That is an absolutely stunning decline, but it just shows the power of interest rates.

Let’s try to put this into real-world terms.

A year ago, the 30-year rate was sitting at 3.66 percent. The monthly payment on a 30-year, $300,000 mortgage at that rate would be $1374.07.

If the 30-year rate rises to 8 percent, the monthly payment on a 30 year, $300,000 mortgage at that rate would be $2201.29.

Does 8 percent sound crazy to you?

It shouldn’t. 8 percent was considered to be normal back in the year 2000…

This is what we are talking about when we talk about the “bubbles” that the Federal Reserve has created. The housing market is now completely and totally dependent on these artificially low mortgage rates. If rates go back to “normal”, the results would be absolutely devastating. But of course the biggest problem with rapidly rising interest rates is the potential for a derivatives crisis.

There are several major U.S. banks that have tens of trillions of dollars of exposure to derivatives. The following is from one of my previous articles entitled “The Coming Derivatives Panic That Will Destroy Global Financial Markets“…

JPMorgan Chase

Total Assets: $1,812,837,000,000 (just over 1.8 trillion dollars)

Total Exposure To Derivatives: $69,238,349,000,000 (more than 69 trillion dollars)

Citibank

Total Assets: $1,347,841,000,000 (a bit more than 1.3 trillion dollars)

Total Exposure To Derivatives: $52,150,970,000,000 (more than 52 trillion dollars)

Bank Of America

Total Assets: $1,445,093,000,000 (a bit more than 1.4 trillion dollars)

Total Exposure To Derivatives: $44,405,372,000,000 (more than 44 trillion dollars)

Goldman Sachs

Total Assets: $114,693,000,000 (a bit more than 114 billion dollars – yes, you read that correctly)

Total Exposure To Derivatives: $41,580,395,000,000 (more than 41 trillion dollars)

That means that the total exposure that Goldman Sachs has to derivatives contracts is more than 362 times greater than their total assets.

The largest chunk of those derivatives contracts is made up of interest rate derivatives.

I have mentioned this so many times before, but it bears repeating that there are approximately 441 trillion dollars worth of interest rate derivatives sitting out there.

If rapidly rising interest rates suddenly cause trillions of dollars of those bets to start going bad, we could potentially see several of the “too big to fail” banks collapse at the same time.

If rapidly rising interest rates suddenly cause trillions of dollars of those bets to start going bad, we could potentially see several of the “too big to fail” banks collapse at the same time.

So what would happen then?

Would the federal government and the Federal Reserve somehow come up with trillions of dollars (or potentially even tens of trillions of dollars) to bail them out?

The Federal Reserve has created a giant mess, and when this current low interest rate bubble ends our financial system is going to slam very violently into a very solid brick wall.

As Graham Summers recently pointed out, entrusting Federal Reserve Chairman Ben Bernanke with control of our financial system is like putting a madman behind the wheel of a speeding vehicle…

Imagine if you were in the car with a driver who was going 85 MPH down a road with a speed limit of 35 MPH (this isn’t a bad metaphor as there is absolutely no evidence that QE creates jobs or GDP growth so there is no reason for the Fed to be doing it in the first place).

The guy is obviously out of control. The dangers of driving this fast are myriad (crashing, running someone over, etc.) while the benefits (you might get where you want to go a little faster assuming you don’t crash) are minimal.

Now imagine that the driver turned to you and said, “I’m thinking about slowing down.” Seems like a great idea doesn’t it? But then a mere two minutes later he says “ we need to continue at 85 MPH for the foreseeable future.”

At this point any sane person would scream, “STOP.” The driver is clearly a madman and shouldn’t be let anywhere near the driver’s seat. Moreover, he’s totally lost all credibility and isn’t to be trusted.

That’s our Fed Chairman.

Sadly, most Americans do not understand any of this.

Most Americans have no idea about the immense economic pain that is going to hit us when interest rates go back to normal levels.

All of this could have been avoided, but instead the American people let the central planners over at the Federal Reserve run wild.

When the bubble finally bursts, the official unemployment rate is going to rocket well up into the double digits, millions of families will lose their homes and America will find itself in the middle of the worst economic crisis in modern U.S. history.

Please share this article with as many people as you can. We need to help people understand what is coming so that they will not be blindsided by it.

This article first appeared here at the Economic Collapse Blog. Michael Snyder is a writer, speaker and activist who writes and edits his own blogs The American Dream and Economic Collapse Blog. Follow him on Twitter here.

linkwithin_text=’Related Articles:’

Be the first to comment on "An Economic Nightmare Scenario"