James Hall, Contributor

Activist Post

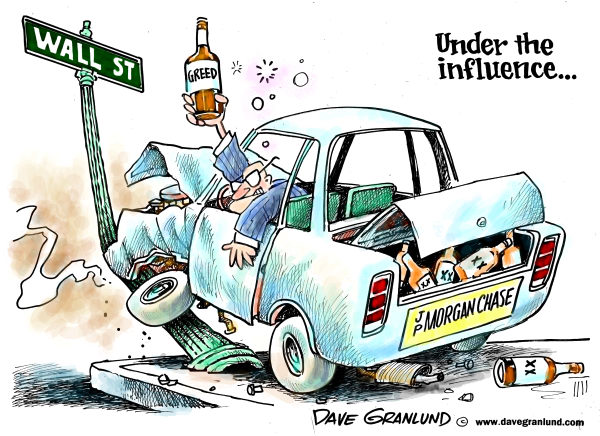

Once again, the practices of the “Too Big to Fail” banksters bring the financial money machine to the brink. The J.P. Morgan derivative losses and trading gambles by their “London Whale” demonstrates business as usual in the murky world of risk distortion. Even the vexing progressive Robert Reich makes an accurate assessment for breaking up the big banks and the resurrecting of Glass-Steagall.

Word on the Street is that J.P. Morgan’s exposure is so large that it can’t dump these bad bets without affecting the market and losing even more money. And given its mammoth size and interlinked connections with every other financial institution, anything that shakes J.P. Morgan is likely to rock the rest of the Street.

Since then, J.P. Morgan’s lobbyists and lawyers have done everything in their power to eviscerate the Volcker rule — creating exceptions, exemptions, and loopholes that effectively allow any big bank to go on doing most of the derivative trading it was doing before the near-meltdown.

The prospects for constructive oversight and judicious safeguards on the money center banks; while, desperately needed, are highly unlikely for enactment. The existing administrative regulation is more about process than accountability. The notice – S.E.C. Opens Investigation Into JPMorgan’s $2 Billion Loss, admits to a limited scope – “Regulators are investigating potential civil violations”.

An important avenue for the S.E.C. investigation, the people said, is the firm’s accounting methods relating to the trades. Investigators could take a close look at a measure known as value-at-risk. The company disclosed earlier this year that it changed the way it calculates the metric, which may have masked some of the risk surrounding this trade. On a conference call Thursday, Mr. Dimon said the firm had reverted to the old way of measuring value-at-risk.

The sociable regulatory atmosphere that turns the revolving door relationship of Wall Street and government regulation is so chummy that only insignificant fines are levied, when the major money center banks gets caught with their hands in the cookie jar. Earnest and comprehensive restructuring of the financial system is impossible as long as the banksters dictate economic policy to their favorite legislative protégés. Fox News identifies the inadequate measures of legislation heralded as a response to prevent future bank bailouts.

Enhanced oversight of derivatives was a pillar of the 2010 financial overhaul law, known as Dodd-Frank, but the implementation has been delayed repeatedly and will not take effect until the end of this year at the earliest.

Both Senator Dodd and Congressman Frank took their retirement after the passage of this banker-friendly diversion from reinstating a total separation of commercial banking from speculative investment banking swap instruments.

Both Senator Dodd and Congressman Frank took their retirement after the passage of this banker-friendly diversion from reinstating a total separation of commercial banking from speculative investment banking swap instruments.

J.P. Morgan Chase, the dominating financial house behind the Federal Reserve, prescribes a coordinated government policy in every political administration. Goldman Sachs best known for supplying senior treasury officials, as Morgan keeps herd on the Fed’s Open Market Committee.

The Washington Times publishes an article, Avast, Wall Street: At J. P. Morgan, there be whales!, and describes practices in the pirate culture that ignores any reform or institutional restraint.

From 2008 onward, taxpayers have been bailing out Jamie Dimon’s J.P. Morgan, along with Citibank, Bank of America, etc., etc., because they’re ‘too big to fail.’ And here goes JPM four years later indulging in the same activities with the same abandon that caused at least two of their major peers to fail in 2008.

‘The London whale’ and his ilk have a distinctly buccaneering attitude out there that should have been tempered by the events of 2008 and the following years. But they haven’t learned a thing, apparently.

Even a casual observer of the unstable international banking environment, knows that the banks game the system at every opportunity. The certified cynic does not need additional proof that the central banks are more important in shaping an unending economic crisis that, favor the “Too Big to Fail” money banks, than governments. If the federal government can enact the Foreign Account Tax Compliance Act to close the door on offshore banking accounts, in theory meaningful revamping of commercial and investment banking should be possible.

Notwithstanding, in practice the banks refuse to allow legislation that strips away the risky trading wagers that contribute to obscene short term paper gains, while sticking the taxpayer and government bail outs when losses accrue.

Mr. Reich continues with a valuable insight on just how the fiasco operates.

And now — only a few years after the banking crisis that forced American taxpayers to bail out the Street, caused home values to plunge by more than 30 percent and pushed millions of homeowners underwater, threatened or diminished the savings of millions more, and sent the entire American economy hurtling into the worst downturn since the Great Depression — J.P. Morgan Chase recapitulates the whole debacle with the same kind of errors, sloppiness, bad judgment, excessively risky trades poorly-executed and poorly-monitored, that caused the crisis in the first place.

Is it possible to save the international financial system from its own greed and high-risk betting patterns?

Is it possible to save the international financial system from its own greed and high-risk betting patterns?

Since it is a matter of time before a financial crisis becomes uncontainable, the judicious alternative is to abandon the entire premise that banking is a debt creation scheme. Any discussion that rejects this axiom is doomed to failure. Coherent oversight means designing a financial system that restricts speculation, leverage and mad risk by requirements of elevated secured capitalization.

Original article archived here

James Hall is a reformed, former political operative. This pundit’s formal instruction in History, Philosophy and Political Science served as training for activism, on the staff of several politicians and in many campaigns. A believer in authentic Public Service, independent business interests were pursued in the private sector. Speculation in markets, and international business investments, allowed for extensive travel and a world view for commerce. James Hall is the publisher of BREAKING ALL THE RULES. Contact batr@batr.org

linkwithin_text=’Related Articles:’

Be the first to comment on "Money Center Banks and Stricter Financial Oversight"