|

| Dees Illustration |

Jason Kaspar

Activist Post

Are there any dollar bulls left? Inflationists across the web are crying ‘victory’ as the dollar sinks and certain asset prices (especially oil prices, food prices, and the gold price) mushroom higher. To the level headed, you should exercise extreme caution against assumed fixed correlations like “weak dollar” means “asset price increases.” Correlations can quickly change.

A mentor of mine consistently preaches that the market will always do whatever it can to make the most investors look foolish. Contrary to conventional wisdom, there is a case that investors should at least consider: that an accelerating decline in the dollar could turn asset prices negative, at least in the short term.

The 1987 crash is an appropriate case study. The cause of that October market crash, when the S&P 500 lost 20.5% in a single day, has never been thoroughly explained. No major event could be credited as the catalyst for such a monstrous and rapid decline.

Portfolio insurance, rapidly rising long term US interest rates, a series of preceding market declines during the week leading up to the crash, and a weakening US dollar are all mentioned as possible triggers. In truth, it was likely a confluence of these and other factors that ultimately pushed the market to a tipping point.

One macro factor stands out among the rest: the rapidly weakening US dollar leading up to Black Monday.

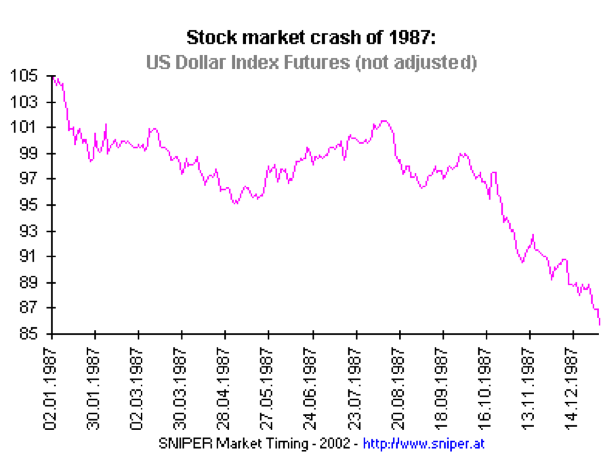

Beginning in late July of 1987, the dollar, after already falling to a seven year low just a few months prior, began a steep decline. A much wider trade deficit than expected was thought to have accelerated the dollar’s descent.

US Dollar: 1987

Over the long term, all things being equal, it is logically sound to conclude that a weakening dollar must cause assets priced in dollars to rise. However, in the short term, markets are not always logical and can anticipate the next move by world bankers. In 1987, the U.S. dollar lost 10% in roughly three months. During the same time span, the equity markets lost close to 30%. Such a move contradicts today’s accepted wisdom.

Though the Federal Reserve has approached its dollar policy with the same restraint as Charlie Sheen at Happy Hour, we should avoid approaching every scenario with broad generalizations, regardless of one’s long term view on the dollar. In the financial markets, nothing goes in a straight line, and correlations tend to break down if certain asset classes move too violently.

US Dollar: Last Twelve Months

While the last twelve months have been unfavorable for the dollar, and while assets have benefited from the Federal Reserve’s currency abuse, correlations do seem to be diverging. Over the past year, the dollar is down roughly 8% and the S&P is up about 9%. But the market has begun reacting more coolly towards a weakening dollar as oil prices have accelerated higher. In fact, in the past two months, the dollar is down 4.25%, and the S&P 500 is down 1%. In the last two weeks, the dollar is down 1.45% and the S&P 500 is down about 1.1%. These moves are in stark contrast to the performance of the past year, so the trend is clearly weakening.

I might worry that if the dollar begins a sharp move downward, the Fed may be forced to approach dollar policy with greater restraint, which could instigate a strong market reaction.

I am fairly agnostic on the dollar’s next move, and I am unsure how that next move will correlate with asset prices. Furthermore, I do not intend to predict an imminent market crash. I simply revisit this history lesson to emphasize a few broader points:

1. Long term correlations do not necessarily equate to the same correlation in the short term.

2. In the short term, crashing asset prices can – and often have – occurred alongside a crashing currency. (This occurred in Europe last year.)

3. Investor sentiment against the dollar is heavily skewed, which should make market observers nervous.

4. The Fed may desire a weaker currency, but it is in their best interest to keep the decline orderly. If a dollar decline were to become chaotic, it would force a Fed reaction that could be unfriendly to the market.

Extreme dollar bears (and asset bulls) should be cautious. The markets do not move in straight lines, and the only certainty in volatile markets is uncertainty. A handy life jacket is worthwhile if the boat flips.

Jason Kaspar is the Chief Investment Officer for Ark Fund Capital Management, focusing on investment and portfolio management. This article first appeared on Gold Shark.

linkwithin_text=’Related Articles:’

Be the first to comment on "Can Dollar Weakness Actually Deflate Asset Prices?"